Making an investment can seem like navigating a maze — and choosing among mutual funds and ETFs (traded price range) is one of the first forks in the road. Both are pooled investment cars that will let you own a slice of an assorted portfolio without selecting individual shares. But below the hood, they paint pretty in a different way. Understanding those differences may help you save money, reduce your tax bill, and align your investments extra carefully with the way you actually live.

What Are Mutual budget?

Mutual finances were around for the reason that the Nineteen Twenties. While you invest in one, your money is pooled with thousands of other investors, and a fund supervisor makes use of that collective capital to buy a portfolio of stocks, bonds, or other property.

The important thing about the function of a mutual fund is how it trades: as soon as, according to day, after the market closes. Regardless of whether you receive your order at 9 a.m. or 3 p.m., you get the same cease-of-day charge, referred to as the internet Asset price (NAV). This simplicity appeals to long-term, hands-off traders who are not looking at the market minute by minute.

Mutual budgets are available in broad types. Actively managed budget rent professional portfolio managers who research and pick out securities as a way to outperform the market. Index mutual price range, popularized by using leading-edge founder John Bogle, without a doubt track a benchmark like the S&P 500 — no stock-choosing worries.

What Are ETFs?

ETFs arrived at the scene in 1993, and feature exploded in recognition due to the fact that. Like mutual finances, they keep a basket of belongings. But unlike mutual funds, ETFs trade on stock exchanges in the course of the day, similar to stocks of Apple or Tesla. You can buy at 10:15 a.m. and promote at 2:forty seven p.m. in case you choose.

Most ETFs are passively managed, tracking an index, area, commodity, or even a selected funding subject matter — the whole thing from smooth electricity to artificial intelligence. A smaller but developing class of actively controlled ETFs additionally exists.

Due to their structure, ETFs normally require a brokerage account to purchase, and you buy them on the cutting-edge marketplace price instead of at the close-of-day NAV.

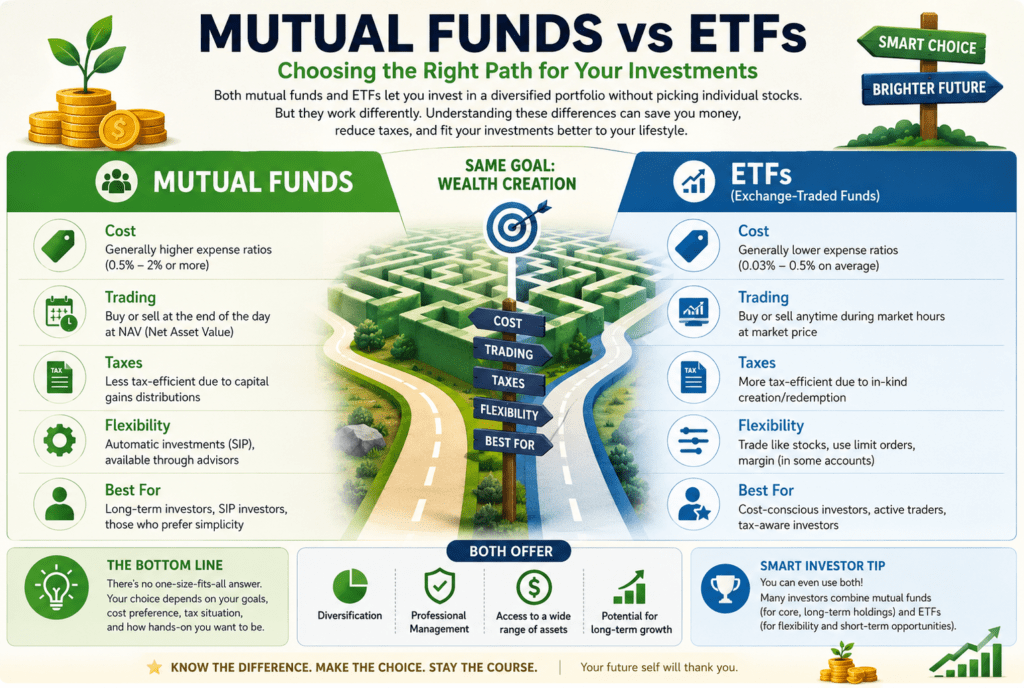

Key differences: A aspect-through-side appearance

Price

Fee is wherein ETFs have historically had the upper hand. The expense ratio — the yearly rate charged as a percent of your investment — has a tendency to be lower for ETFs than for actively managed mutual funds. Many extensive-marketplace ETFs price as little as zero.03% in line with year, which means you pay just $3 annually on a $10,000 funding.

Actively controlled mutual funds typically charge between 0.5% and 1.5%, and some pass better. Over the decades, this distinction compounds notably. A 1% gap in annual expenses can cost you tens of thousands of bucks on a long-term portfolio.

That said, index mutual funds have grown to be enormously aggressive. Vanguard, constancy, and Schwab all offer index mutual price range with expense ratios corresponding to — or in a few instances identical to — their ETF opposite numbers. So the fee gain of ETFs is maximum stated while comparing them to actively managed mutual funds.

Tax efficiency

That is wherein ETFs shine structurally. Due to a mechanism known as the “in-type advent and redemption” procedure, ETFs do not often distribute capital gains to shareholders. While traders promote an ETF, stocks are clearly offered on the open marketplace — the fund itself does not need to sell its underlying holdings to fulfill redemptions.

Mutual price range, especially actively controlled ones, often sell securities inside the portfolio to fulfill redemptions or rebalance holdings. That income can cause capital profits distributions, which might be passed on to all shareholders — even folks who failed to sell a proportion. You could owe taxes on profits you by no means individually realized.

in case you’re investing in a taxable brokerage account, ETFs are generally more tax-friendly. In a tax-advantaged account like an IRA or 401(ok), this distinction subjects a long way less.

Trading Flexibility

ETFs offer intraday buying and selling, which means that you could purchase or sell at any point during market hours and use advanced order types like restriction orders or prevent losses. For active traders or tactical traders who want to respond to market activities in real time, this pliability is valuable.

For most long-term traders, however, intraday buying and selling is a double-edged sword. The ease of purchasing and promoting can encourage emotional, reactive choices — exactly the conduct that erodes long-term returns. Mutual finances’ once-every-day pricing can act as an integrated circuit breaker against impulsive buying and selling.

Minimal Investments

Mutual budgets often require a minimum initial investment, from time to time, $1,000 or more, although many fund households have reduced or removed minimums in recent years. ETFs, with the aid of evaluation, may be purchased for the price of a single proportion — and with fractional share making an investment now presented via maximum primary brokers, you could begin with as low as $1.

This makes ETFs especially available for brand-spanking-new investors who’re just getting started.

Computerized investing

One location in which mutual price range maintains a clean gain is computerized investing. maximum fund corporations can help you set up routine purchases of a set dollar amount — say, $200 every month — at once into a mutual fund. This makes dollar-fee averaging convenient and maintains investing on autopilot.

Computerized making an investment in ETFs is possible through a few agents, however is not as universally supported. In case you want to “set it and forget it,” a mutual fund may be the greater frictionless desire.

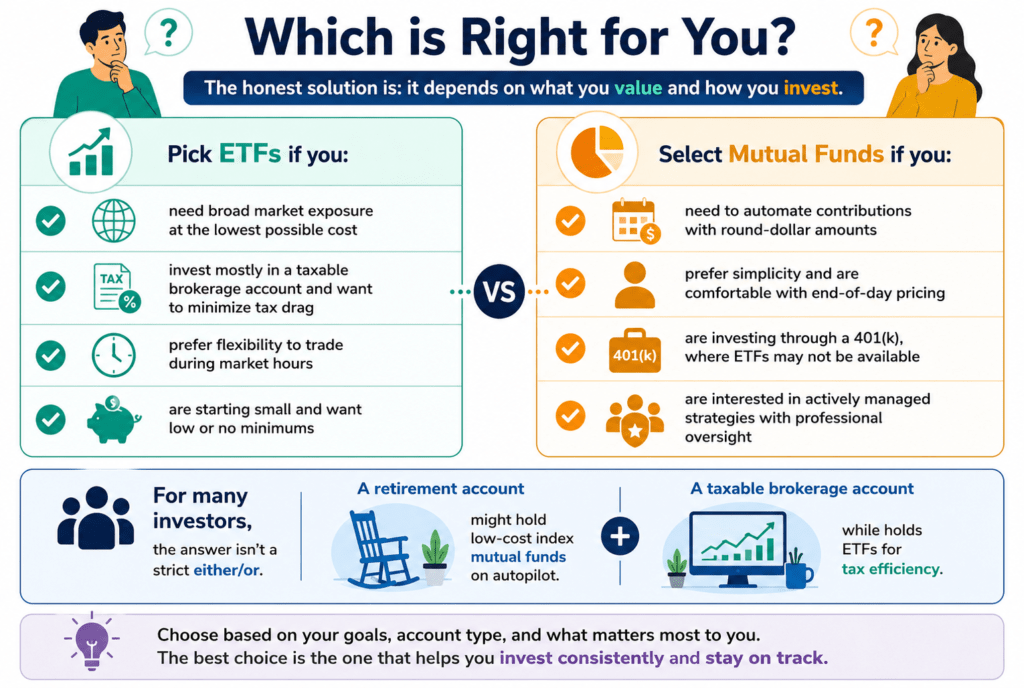

Which is right for you?

The honest solution is: it relies upon what you cost and how you make investments.

Pick ETFs if you:

- need vast marketplace publicity at the bottom viable value

- Invest in the whole in a taxable brokerage account and want to minimize tax drag

- decide on flexibility to alternate at some stage in marketplace hours

- Are beginning small and want low or no minimums

Select mutual funds if you:

- need to automate contributions with spherical-dollar amounts

- choose simplicity and are secure with give up-of-day pricing

- Are investing through a 401(ok), wherein ETFs might not be available

- Are inquisitive about actively controlled techniques with professional oversight

for many buyers, the solution isn’t a strict either/or. A retirement account might preserve low-value index mutual funds on autopilot, while a taxable brokerage account holds ETFs for tax efficiency.

Conclusion

Both mutual funds and ETFs are valid, effective gears for constructing wealth. The variations that depend the most come right down to value, taxes, buying and selling behavior, and convenience. For most people of ordinary buyers with long-term horizons, a low-price index ETF or index mutual fund will serve them similarly well.

Attention much less on the wrapper and more on what’s inside: diversification, low charges, and the ability to stay invested thru marketplace usaand downs. That aggregate — irrespective of the vehicle — is what builds lasting economic safety.