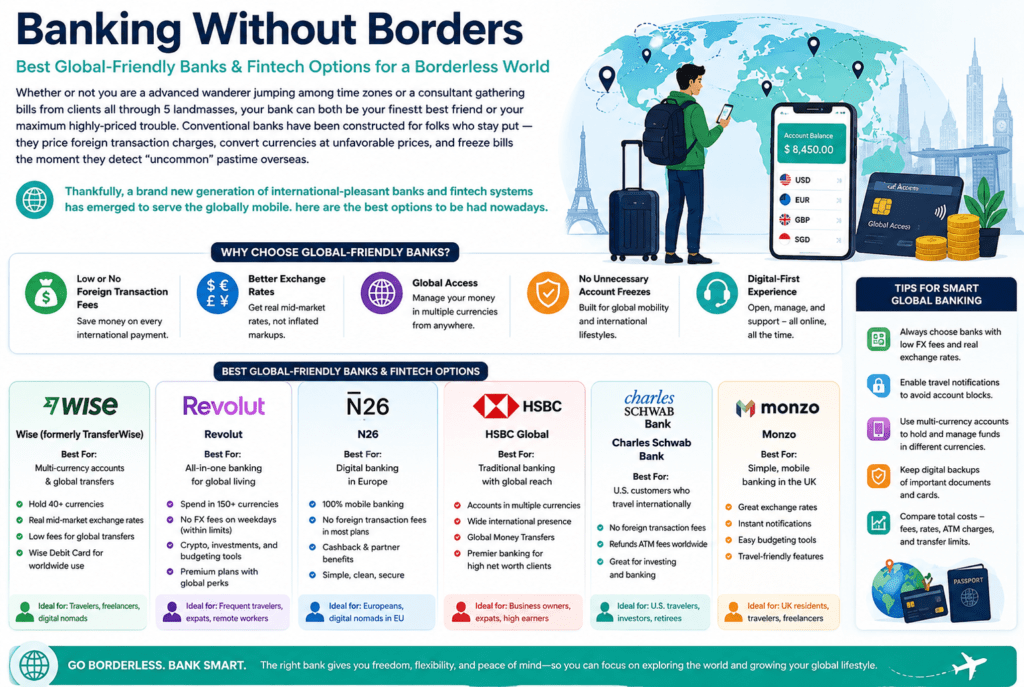

Whether or not you are an advanced wanderer jumping among time zones or a consultant gathering bills from clients all over 5 continents. Your bank can both be your best friend and your most expensive trouble. Conventional banks have been constructed for folks who stay put — they charge foreign transaction fees. Convert currencies at unfavorable prices, and freeze bills the moment they detect “unusual” activity overseas. Thankfully, a brand new generation of international-friendly banks and fintech systems has emerged to serve the globally mobile. Right here are the best options to be had nowadays.

Clever (formerly TransferWise)

First-class for: Receiving global payments and multi-forex control

Smart is arguably the gold standard for freelancers operating with worldwide clients. Its multi-currency account helps you to keep money in over 50 currencies and receive payments via neighborhood financial institution information within the US, UK, EU, Australia, Canada, and several other markets. Which means your American consumer will pay you like a local, fending off steeply-priced global card costs on their stop too.

The real draw is Wise’s change charge. not like conventional banks that pad their charges with hidden margins, clever uses the mid-market fee and price a small, transparent price. Over the years, this has provided significant financial savings. The clever debit card works in over a hundred and fifty nations, and the first ATM withdrawals per month (as many as a restriction) are free.

For freelancers, the enterprise account is particularly effective, allowing invoicing, batch payments, and integration with accounting software. The handiest disadvantage: sensible isn’t always a conventional financial institution in most jurisdictions, so deposits might not be covered by means of widespread government coverage schemes depending on your country.

Revolut

Excellent for: travelers who want an all-in-one financial app

Revolute started out as a journey card and has grown right into a full-featured neobank with operations throughout Europe, the United States, Australia, and beyond. For vacationers, it’s hard to conquer. Exchange currencies at interbank charges (within month-to-month limits at the loose plan), pay abroad with no overseas transaction fees. And manipulate everything from a slick cell app.

The top rate and metallic tiers offer better ATM withdrawal limits, higher trade charge allowances, travel coverage, and living room access. And cashback — making them simply competitive with conventional premium travel credit cards. Revolut additionally supports cryptocurrency, inventory buying and selling, and savings vaults. This appeals to freelancers who want to consolidate their finances in one place.

One caveat: Revolut’s customer support has traditionally been patchy, and the platform’s availability varies extensively by means of use. s. It is strongest in Europe and works properly inside the UK, but US users get a barely stripped-down experience.

Charles Schwab financial institution

nice for: US-based totally tourists searching for 0-charge ATM get right of entry to worldwide

For individuals, Charles Schwab’s Excessive Yield Investor bank account is something of a legend among long-term travelers. It reimburses all ATM prices globally — every one, without a month-to-month cap — and prices with no overseas transaction costs. The account calls for a related Schwab brokerage account that is loose and smooth to open.

Schwab operates like a proper financial institution with FDIC coverage, which gives it an edge over many fintech alternatives. The trade price implemented for overseas currency transactions is competitive, even though no longer pretty on the mid-market level of sensible or Revolut. For freelancers based inside the US who need reliable cash access everywhere in the world, Schwab is an almost unbeatable base account.N26

N26

Satisfactory for: ECU freelancers and digital nomads

N26 is a German cellular financial institution licensed in the EU. Because of this, purchaser deposits are covered under European deposit guarantee schemes — a reassurance that many fintech alternatives cannot provide. It operates in most EU nations and chooses markets globally, with a clean interface and sturdy journey features.

The unfastened account includes a credit card and not using a foreign transaction costs. Paid degrees (smart, You, and metallic) upload tour insurance, companion discounts, and higher ATM withdrawal limits. N26 You, specifically, is designed with travelers in mind, bundling scientific and trip cancellation coverage that can replace standalone travel insurance.

For eu-based totally freelancers, N26 additionally gives a business account with cashback on purchases and easier fee tracking. the principle issue is geographic: N26 is basically unavailable within the US and has limited attain out of doors Europe.

Payoneer

First-rate for: Freelancers on fundamental structures like Upwork, Fiverr, and Amazon

Payoneer isn’t always a bank in the traditional sense, but for freelancers, it functions as one. It’s the charge spine at the back of structures like Upwork, Fiverr, Airbnb, and Amazon Marketplace. Permitting users to obtain payments in more than one currency through neighborhood receiving bills, similar to clever.

Where Payoneer shines is its deep integration with the freelance economic system. Many universal clients and marketplaces pay out at once to Payoneer accounts, as often as possible at no additional cost. You could withdraw to a nearby bank account, spend via the Payoneer Mastercard, or make business payments to other Payoneer users.

The prices are truly better than clever for currency conversions, and the platform is more utilitarian than polished; however, for freelancers whose clients specifically use Payoneer, it is fundamental.

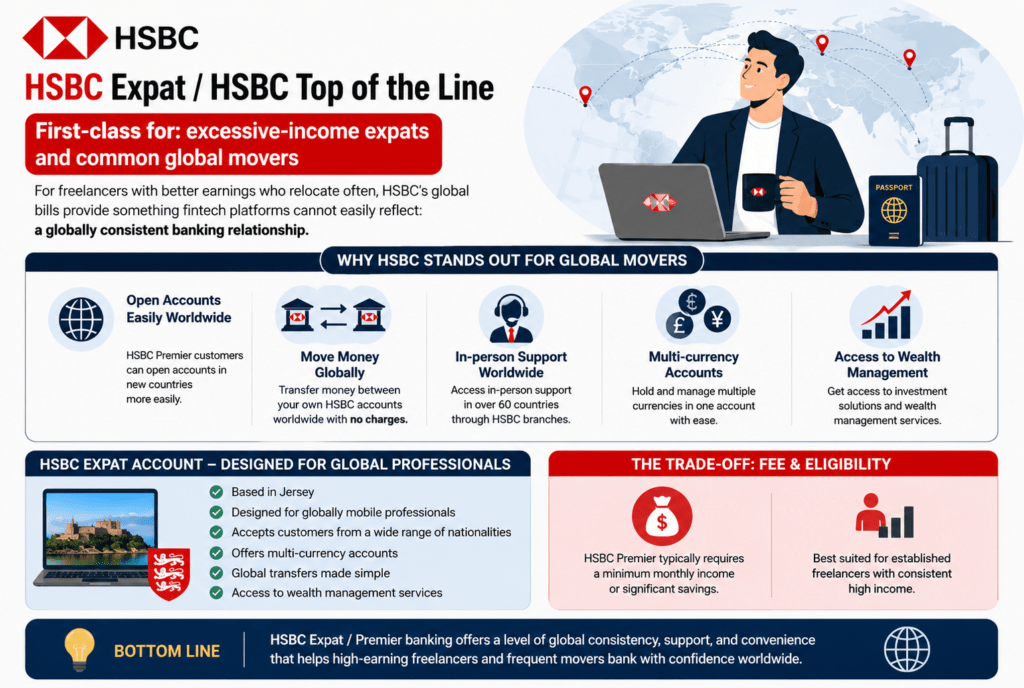

HSBC Expat / HSBC top of the line

First-class for: high-income expats and common global movers

For freelancers with better earnings who relocate often, HSBC’s global bills provide something fintech platforms cannot easily reflect. A globally consistent banking relationship. HSBC’s greatest customers can open accounts in new nations more easily. Awitch money among their own HSBC accounts globally without charges, and get access to in-person aid in over 60 nations.

The HSBC Expat account, primarily based in Jersey, is designed specifically for the world-over mobile experts and accepts customers from an extensive range of nationalities. It offers multi-forex bills, global transfers, and get admission to to wealth control services.

The alternative is fee and eligibility. HSBC is most desirable, usually calls for minimal monthly profits or huge financial savings. Making it more proper to established freelancers with constant high profits as opposed to those simply starting out.

The way to pick out the right one

No single bank works perfectly for every person. The proper combination relies upon some key elements:

- Where your customers are — If the maximum of your profits arrives in USD or EUR, Smart or Payoneer will save you the maximum on conversions.

- where you stay and journey — Charles Schwab fits US-based travelers; N26 is better for Europeans; Revolut works nicely throughout both.

- How tons you earn — high earners advantage from HSBC’s top-class services; lean-finances tourists get incredible cost from Schwab or a free Revolut account.

- Whether you need deposit insurance — If that topic, stick with licensed banks like N26, Schwab, or HSBC.

The best method most seasoned freelancers and travelers use is a combination. A sensible or Payoneer account to receive client bills cost-effectively, paired with a Schwab or Revolut card for spending and ATM withdrawals on the street. Together, they cover almost every financial need without the punishing charges that traditional banks have charged for decades.

The sector is your office. Your bank needs to act like it.