Scope can seem like a labyrinth of troublesome expressions and extraordinary print. But one term you essentially require to secure is legitimate obligation scope. Whether or not it applies to your vehicle protections, residential scope, or commercial endeavor scope, legitimate duty scope is one of the most basic securities you seem to have — and one of the most misunderstood.

Allow it down in plain language.

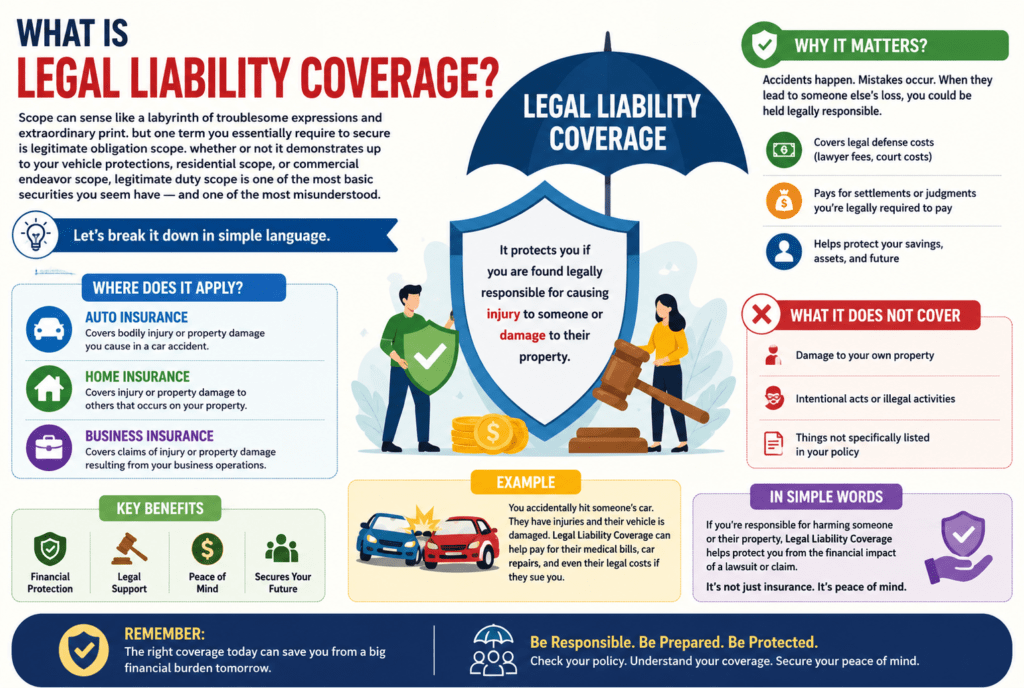

What’s risk coverage?

At its center, the lawful obligation scope is protection that pays for harm you cause to somebody else.

Think approximately it this way: if you incidentally harmed somebody or hurt their possessions, they are able to hold you legally liable. That implies they are able to sue you, take you to court, and likely claim cash from you. Obligation protections step in to address those costs — so that you do not have to pay out of your own pocket.

It does not cover your individual mishaps or your exceptionally valuable assets. It’s particularly planned to watch other individuals besides you, and to watch your accounts in that manner.

A simple instance

Consider you’re riding and you run a pink mellow, smashing into any other car. The converse method of reasoning drives is hurt, and their car is annihilated. You are at fault.

Now that other driving drive has clinical bills, reestablish costs, and likely lost compensation if they cannot go to canvases. Without the lawful obligation scope, you must pay all of that yourself. With obligation scope, your protection trade endeavor will pay the costs on your behalf, up to your scope limits.

Simple, adequate, appropriate? Presently, let’s look at where legitimate duty protections show up and what it truly covers.

Where does the scope of lawful obligation apply?

Legal obligation scope is proposed in a few forms of scope regulations.

- Car coverage

When you control a car, most nations and states legally require you to carry liability protection. It covers physical harm and the harm you cause to others in a bend of destiny. in case you harm an individual or demolish their vehicle, this is what pays for it.

- Home protections (property owner’s or Renter’s insurance)

This covers you if an individual gets harmed on your property. Say a visitor slips on your damp floor or your canine chomps a neighbor. Your house risk scope will pay for his or her legal bills and any jail costs in the event that they choose to sue.

- Business insurance

Agencies confront legitimate duty perils every single day. A client should slip into your spare, a benefactor may need to pronounce your counsel brought approximately them monetary misfortune, or an item you advertised may need to harm somebody. Trade risk scope — regularly known as wellknown lawful obligation protections — secures the trade undertaking from those forms of claims.

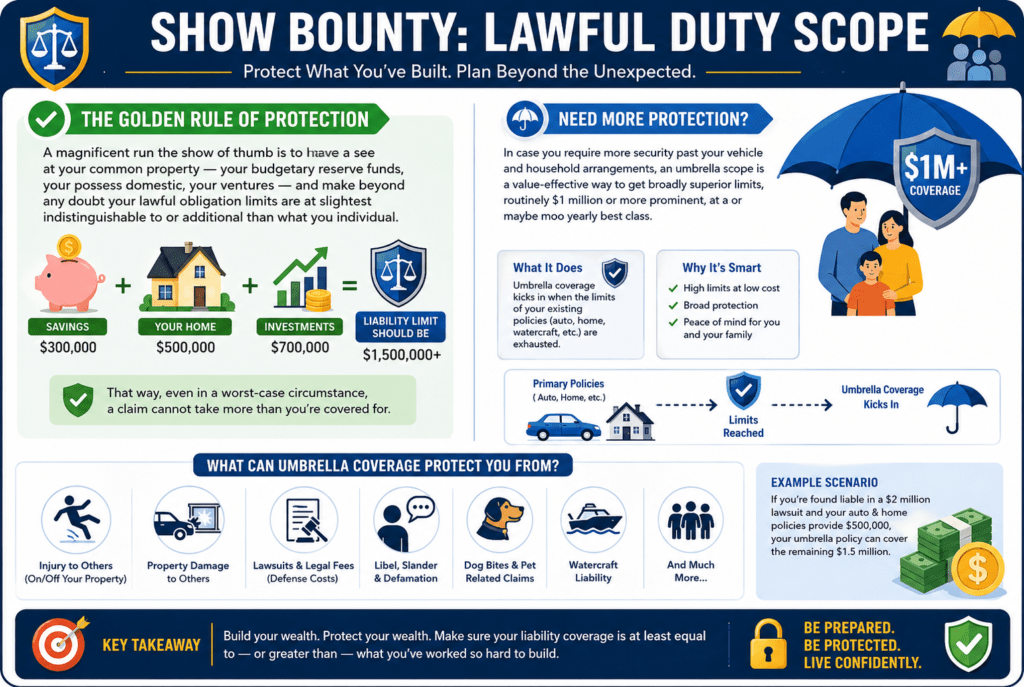

- Umbrella insurance

That is a assist layer of risk security that kicks in when your stylish vehicle or household arrangement limits run out. It is like a security web on beat of your other rules, more often than not veiling colossal claims that may in any other case wipe out your savings.

The 2 imperative sorts of risk insurance

While you consider a legitimate duty arrangement, you may commonly see two classes:

- Bodily damage liability

This covers clinical costs, lost compensation, and lawful offense costs in case you harm any other person. It is able to, in addition, cover throbbing and persistent claims if the hurt party sues.

- Property harm legitimate responsibility

This covers the cost to repair or supplant an individual’s resources that you harmed. In a vehicle accident, this will recommend buying the elective rationale force’s car support. In a domestic state of undertakings, it would propose paying to reestablish a neighbor’s fence that your tree fell on.

What are scope Limits?

Legal obligation protections don’t cover boundless amounts. Every method has a constraint — the maximum amount your protection company can pay for a single announcement or within a scope period.

You may regularly see limits composed like this: 100/300/one hundred

Right here’s what those numbers recommend for car liability:

- $one hundred,000 – most extreme in line with man or lady for substantial injury

- $three hundred,000 – most in line with mischance for physical harm (total)

- $100,000 – most for asset damage

If the harms surpass your scope limits, you are, in my supposition dependable for the unwinding. That is why selecting the right limits subjects — going for the cheapest, least protections can leave you genuinely uncovered.

What risk protections no longer encompass

It makes a difference to be clear about what risk does not cover:

- Your exceptional mishaps — your individual logical bills after a coincidence you caused aren’t ensured with the help of liability. You’ll need partitioned logical bills or non-public harm assurance scope for that.

- Your individual vehicle or assets are hurt — in case you crash into a divider, risk won’t repair your vehicle. That is what collision scope is for.

- Intentional acts — if you purposely hurt a person’s assets or harm somebody, the scope may not cover it.

- Crook fines or results — lawful obligation protections cover respectful claims, presently not criminal prices.

Why is the legitimate duty scope so vital?

Human creatures habitually belittle how rapidly charges can transfer up after a bend of destiny. A single car mishap can result in tens of thousands of dollars in therapeutic bills. A claim can effectively climb into the masses of thousands. Without an obligation scope, the costs come straightforwardly from your monetary investment funds, your domestic value, or your predetermination income.

Liability protections basically act as a financial shield. It stands among you and monetary harm, whereas something is going wrong — indeed, if it turned into a fair mistake.

That is why most financial advisors and protection experts propose wearing more than the minimum. The negligible required by way of control is as often as a few as separate, and more to cover real-global fees.

How bounty lawful duty scope do you want?

A magnificent rule of thumb is to have a look at your common property — your budgetary reserve funds, your personal domestic, your ventures — and make beyond any doubt your legal obligation limits are at least indistinguishable to or additional than what you own. That way, indeed in a worst-case circumstance, a claim cannot take more prominent than you’re secured for.

In case you require more security beyond your vehicle and household arrangements, an umbrella scope is a value-effective way to get broadly superior limits, routinely $1 million or more, at a low or maybe zero yearly premium.

Conclusion

Legal obligation protections aren’t continuously around defensive things — it is almost protecting people (and protecting yourself from the financial results whereas a individual gets hurt). It’s miles the spine of most protection rules and, in parts of places, is legitimately required for a motive.

knowing what legitimate duty protections are, what they can pay for, and what kind of places you require puts you in a million more grounded position to make intelligent scope choices. Don’t hold up until something is going inaccurate to decide whether or not you have sufficient. Outline your protections nowadays, and make certain the limits reflect your genuine financial situation.

Due to the reality, where mishaps show — and that they do — the remaining component you require is to be stuck without a security net.