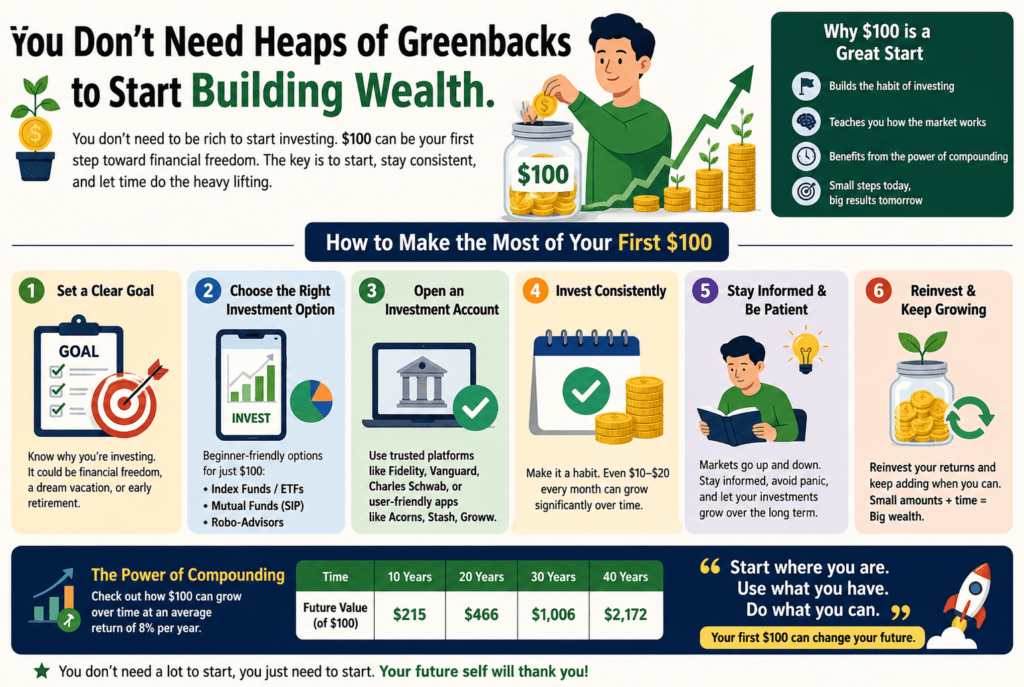

You don’t want heaps of greenbacks to start constructing wealth. The notion that making an investment is best for the wealthy is one of the most persistent and unfavorable monetary myths out there. The truth is that $one hundred — a sum the majority can scrape together within a month or two — is a wonderfully valid place to begin. What matters a long way more than how much you start with is what you actually start.

Right here’s how to make the most of your first $one hundred.

Apprehend what you’re operating with

Before putting a single dollar everywhere, take five minutes to comprehend the fundamentals. making an investment manner, placing your cash into belongings — shares, price range, bonds, or other instruments — with the expectancy that they will grow in cost through the years. not like saving, which preserves money, investing multiplies it (and sure, it carries a threat).

Your $a hundred won’t make you rich in a single day. However invested consistently and wisely, it is able to grow significantly over the years via the energy of compound interest — the procedure wherein your returns earn their own returns. A $one hundred funding growing at 10% annually will become kind of $1,745 in 30 years without adding any other cents. Add $one hundred every month, and that range balloons beyond $2 hundred,000.

The maximum treasured asset you have right now isn’t your cash. It’s been a while.

Deal with the basics first

Before investing, make certain you are not setting yourself up to fail. Ask yourself quick questions:

Do you have excessive-interest debt? Credit card debt at 20%+ is a guaranteed -20% return on your money. Paying that off first is the pleasant funding you can make. Exceptions: low-interest debt (pupil loans, car payments) can coexist with making an investment.

Do you have any emergency financial savings? Even a small buffer of $300–$500 in a savings account prevents you from having to sell your investments the moment existence throws a curveball.

if you’re clean on both, your $100 is ready to work.

Open the proper Account

The account type topics are as plentiful as what you spend money on, because taxes quietly erode returns over the years.

Roth IRA — when you have earned profits, that is frequently the neatest first account. You make contributions after-tax greenbacks, your money grows tax-free, and you pay zero tax while you withdraw in retirement. In 2025, you could make a contribution up to $7,000 consistent with the year. Your $100 fits with ease right here.

Traditional IRA — Contributions can be tax-deductible now, but withdrawals in retirement are taxed as income. A strong option if you expect to be in a lower tax bracket later.

organisation 401(ok) — in case your organisation gives a fit, make contributions enough to capture it before doing whatever else. A 50% healthy to your contributions is an instantaneous 50% move returned — nothing beats that.

Taxable brokerage account — No tax advantages, however, no restrictions either. Extremely good for making an investment past your IRA limits or for dreams before retirement age.

Maximum main structures — fidelity, Charles Schwab, and others — permit you to open an IRA or brokerage account without a minimum deposit. You may start with precisely $one hundred.

Choose what to spend money on

With $100, you need simplicity and occasional fees, notably otherwise. Here are the excellent options:

Index finances and ETFs

An index fund or ETF (alternate-Traded Fund) is a unmarried investment that holds masses or heaps of shares right now, monitoring a marketplace index just like the S&P 500. Rather than betting on one organisation, you’re having a bet at the broad marketplace — and traditionally, the market goes up over the years.

Look for finances with price ratios beneath 0.20%. Pinnacle selections encompass:

- VTI (Vanguard Overall Stock Market ETF) — covers the whole U.S. marketplace

- FXAIX (Fidelity 500 Index Fund) — no minimum investment, zero.1/2% cost ratio

These are easy, diverse, and conflict-examined. Most of the world’s most sophisticated traders — along with Warren Buffett — advise index budget for everyday investors.

Fractional shares

Want to own a piece of Amazon, Apple, or Google, but can not have enough money for a full share? Maximum contemporary brokerages now offer fractional stocks, letting you purchase a slice of a stock for as low as $1. This makes it possible to diversify throughout huge-name companies inspite of $a hundred.

Robo-Advisors

If you’d alternatively no longer consider it at all, a robo-advisor like Betterment or Wealthfront will make investments with your money automatically based on your age and risk tolerance. They charge a small annual price (usually 0.25%) and deal with the whole lot from portfolio selection to rebalancing. It is a palms-off, sensible choice for authentic novices.

Make it a dependency

Your $100 investment topics, however, your $100-in line with-month habit topics are a long way more. Here’s the way to build it:

Automate contributions. Install an automated switch — even $25 or $50 a month — into your investment account. Automation eliminates willpower from the equation. You make investments before you spend, no longer after.

Don’t chase warm shares. The stock that doubled in the closing year is the day before today’s information. Trying to pick winners constantly is something even professional fund managers fail at. Stick to your index finances.

Stop watching the market day by day. Quick-term market swings are noise. Checking your account each day is a fast way to make emotional decisions you may regret. Test quarterly. Assume in decades.

Increase contributions each time possible. got a improve? Direct half of it in the direction of investments earlier than your lifestyle expands to soak up it. This one addiction builds more wealth than nearly anything else.

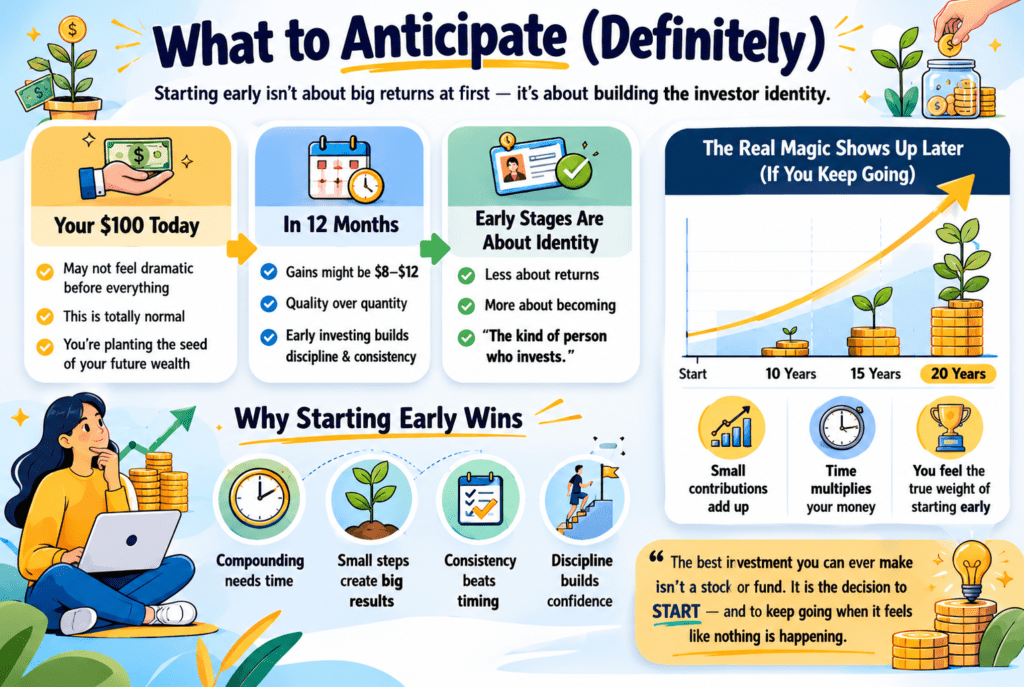

What to anticipate (definitely)

Your $100 may not feel dramatic before everything. In 12 months one year, the gains might be $8–$12. That is quality. Investing inside the early tiers is less about the returns and more about constructing the identity of a person who invests.

The real magic suggests itself later. At the ten, 15, 20-12 months mark — in case you’ve kept contributing — you may take a look at your account stability and experience the overall weight of what starting early truely supposed.

The exceptional funding you may ever make isn’t a particular inventory or fund. It is the selection to start — and to keep going, whilst it looks like nothing is happening.

Conclusion

- Pay off any credit card debt first

- Set apart a small emergency cushion

- Open a Roth IRA or brokerage account (Constancy or Schwab are tremendous starting points)

- invest your $one hundred in a low-value S&P 500 index fund

- set up computerized monthly contributions, although small

- depart it on my own and permit time to do the work

Investing entails risk, consisting of the possible lack of importance. This newsletter is for academic purposes and isn’t always a personalised financial recommendation. Remember consulting an authorized economic planner for guidance tailor-made in your situation.