Researcher contract obligation remains one of the most squeezing money related burdens confronting millions of indebted individuals. With the display of absolution applications exchanging significantly in recent years. By means of court decisions, authoritative changes, and exchanging organizations, it can be difficult to realize where you stand. Here is a clean-eyed breakdown of what researcher advance absolution looks like these days, who qualifies, and what to watch out for.

The colossal picture: in which things stand in 2026

The period of colossal, clearing exculpating is by and large over, as a minimum for now. The Biden administration’s most striking abstinence activity, the spare (Sparing on a valuable tutoring) arrangement, was struck down by means of the courts. As of Walk 2025, a court administering coordinated the department of preparing to halt forcing store completely. Influencing hundreds of thousands of borrowers who had selected or arranged to sign up. The department began informing indebted individuals in early 2026, giving them a 90-day window to select an unused repayment plan.

What remains are more focused on, longer-status applications — and that they, in any case. Offer critical ease if you recognize how to utilize them.

Applications that might be lively in any case

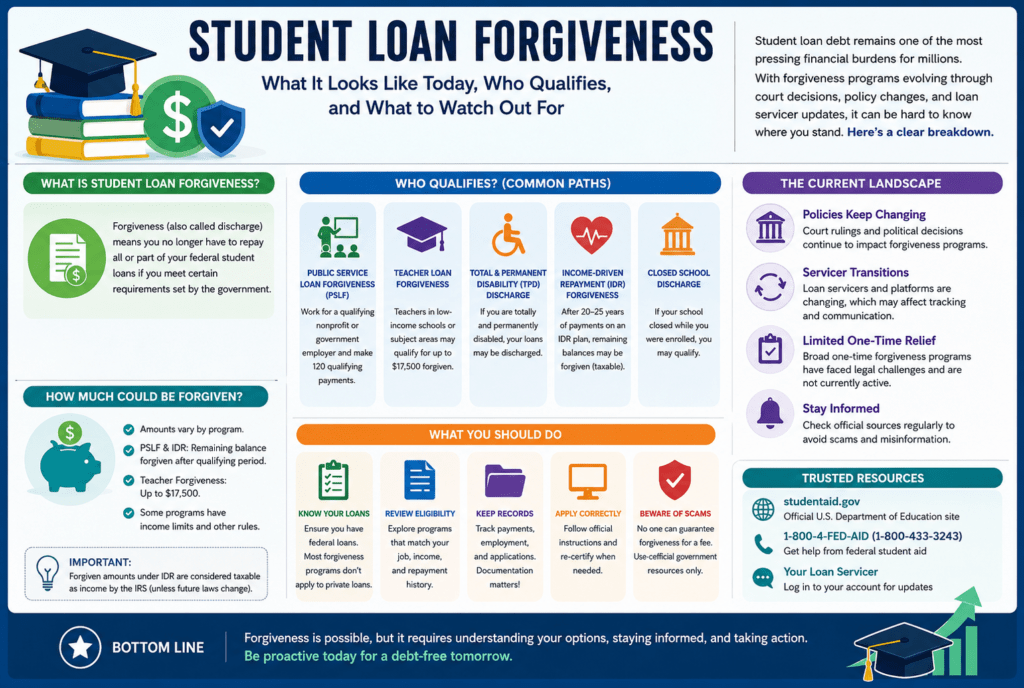

- Public carrier contract Pardoning (PSLF)

PSLF is ostensibly the most viable absolution application, but it is also totally operational. It wipes out remaining government contract equalizations after 120 qualifying month-to-month installments — it’s 10 years. For borrowers working full-time in qualifying open supplier or nonprofit occupations. Teachers, medical attendants, specialists, workers, and social representatives are among the people who ordinarily gain.

The great news: PSLF absolution remains tax-free under government control, a gigantic advantage compared to other kinds.

- Earnings-driven emolument (IDR) Forgiveness

Income-based repayment (IBR), income-Contingent reimbursement (ICR), and Pay As You Win (PAYE) plans are, in any case, accessible. Underneath these plans, month-to-month bills are capped at a rate of your optional benefits. And any extreme balance is forgiven after 20 to 25 a long time of qualifying payments.

In October 2025, following a criminal suit brought by the Yank League of instructors, the office of instruction concurred to recharge allowing contract release for borrowers who total the indicated bills underneath IBR, PAYE, and ICR plans — a monster win for borrowers who have been left in uncertainty.

One critical caveat: the branch’s cost following gadget was taken down in April 2025 and has presently not been reestablished. In case you require a redesign in your qualifying installment plan, contact your contract servicer clearly — they must have a record of your payments.

Trainer advance Forgiveness

Instructors who work five continuous years in a low-earnings workforce or instructional career enterprise can moreover qualify for up to $17,500 in pardoning on beyond any doubt government credits. This application remains dynamic, and the absolution is, by and large, tax-free.

Total and lasting inadequacy (TPD) Discharge

Absolution underneath TPD was tax-free through 2025; the assess treatment for releases going on in 2026 and past depends on the exact events and might require an interview with a tax professional.

A primary unused improvement: the repayment help Arrange (RAP)

One noteworthy interchange on the skyline is the rollout of the repayment assistance Plan (RAP), expected in July 2026. RAP may also increase reimbursement timelines up to 30 days for a few indebted individuals. Indeed, as it might diminish month-to-month bills, a longer reimbursement window would result in more side interest paid over the long term — and possibly a bigger excused soundness that would be subject to tax. Borrowers considering approximately RAP are required to form the lengthy-time period cost carefully before enrolling.

The Survey trap: What ought to Hit Your wallet

That is where various obliged people are caught off guard. For a long time, most government understudy contract exculpating was ensured from government benefit charges underneath the Yank Ensure Orchestrate Act (ARPA). That security connected to absolution was prepared through December 31, 2025, and it has presently expired.

Starting in 2026, pardoning procured under earnings-driven repayment plans is ordinarily treated as assessable income. That implies if $50,000 of your contract’s solidness is pardoned, the IRS may also treat that $50,000 as typical wage for the 12 months it was canceled. Depending on your assess bracket, this can create a monster assessment charge — once in a while known as a “charge bomb.”

Exceptions stay. PSLF pardoning, teachers’ contract Pardoning, and greatest incapacity releases proceed to be tax-unfastened underneath isolated government arrangements. The charge change essentially impacts long-term IDR forgiveness.

What to do presently: if you are looking ahead to absolution in 2026 or afterward, arrange in progress. Bear in mind developing your assess withholdings, making anticipated quarterly tax installments, or putting separated budgetary reserve funds extraordinarily for a capacity charge legitimate responsibility.

What passed off to the spare Plan?

The store arrangement turned into the Biden administration’s greatest liberal earnings-driven remuneration elective, Providing diminish charge caps and speedier pardoning timelines than older IDR plans. It got to be blocked by way of the 8th Circuit court of Appeals in Admirable 2024 after a mission from a fusion of Republican-led states. An exceptionally final court administering in Walk 2025 finished this system.

If you were selected in the shop, you’ll be transitioned to an unmistakable remuneration arrange see ahead to communications from your credit servicer. And take development inside any said closing dates to maintain a strategic distance from being placed into a default reimbursement arrange that won’t improve your financial situation.

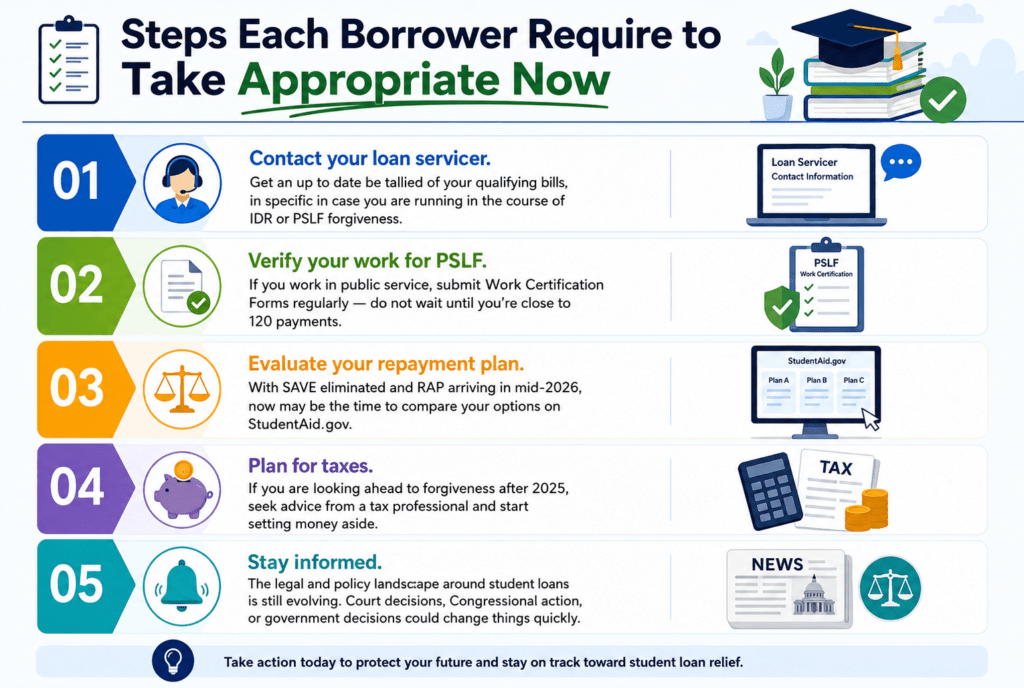

Steps each Borrower requires to take appropriately now

Contact your contract servicer. Get an up to date be tallied of your qualifying bills, specifically in case you are running in the course of IDR or PSLF forgiveness.

- Verify your work for PSLF. In case you work in an open supplier, distribute Work Certification forms frequently — do not hold up until you’re close to one hundred twenty bills.

- Evaluate your stipend arrangement. With the store disposed of and RAP arriving in mid-2026, presently may be the time to compare your choices on StudentAid.gov.

- Plan for charges. If you are looking ahead to absolution after 2025, look for advice from a assess proficient. And start putting cash aside.

- Stay educated. The lawful offense and arrangement scene around student advances is still advancing. court decisions. Congressional movement, or govt choices, ought to trade things quickly.

Conclusion

Student contract pardoning has no longer vanished — but it has risen as a more prominent, complex, and conditional. And in some cases, more accessible. The applications that stay are genuine and truly worth seeking after if you qualify, specifically PSLF and IBR-based forgiveness. Be that as it may, the days of expecting a wide cancellation are over. And indebted individuals who remain detached risk missing basic closing dates or managing with unforeseen charge bills.

The most intelligent circulate right presently seem to be getting educated, getting organized, and taking control of their reimbursement procedure. Your financial future may moreover depend on it.