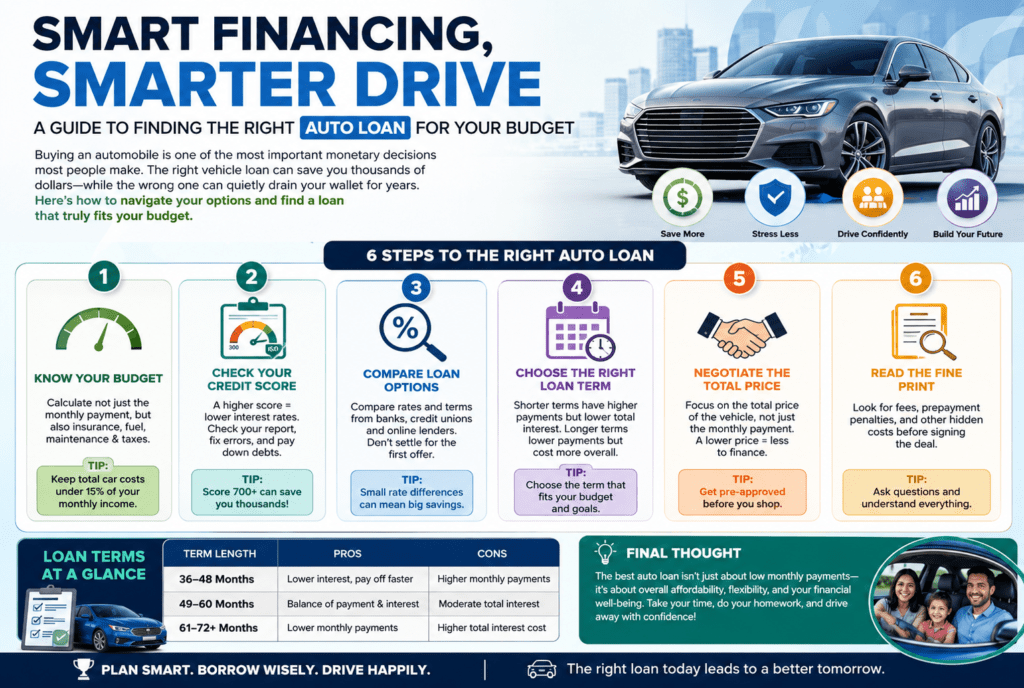

Buying an automobile is certainly one of the most important financial decisions the general public makes, and for most of the people of shoppers, meaning disposing of a loan. The right vehicle loan can save you thousands of greenbacks through the years, while the wrong one will quietly drain your wallet for years. Here’s a way to navigate your alternatives and find a loan that, without a doubt, fits your budget.

Recognize your finances before you walk in

Before you even consider interest costs or mortgage terms, get clear on what you can truly come up with the money for. A commonplace rule of thumb is to hold your overall monthly vehicle prices — mortgage fee, insurance, fuel, and renovation — below 15–20% of your monthly take-home pay.

Start with the aid of listing your month-to-month earnings and fixed expenses. Anything is quite simply left over units on your ceiling. Many shoppers make the mistake of focusing on the month-to-month payment alone, in preference to the overall fee of the loan. A lower month-to-month price can appear attractive, but it frequently means an extended loan term — and a ways extra money paid in interest over the years.

Set a practical target before you start purchasing. This quantity will be your anchor in the course of the entire method.

Understand how car loan interest Works

Car loans use an easy hobby, which means interest is calculated at the outstanding principal balance. Your month-to-month charge remains the same; however, in the early months, a bigger element is going towards interest, and in later months, more goes towards the principal.

The key determinant of attention is the yearly percentage rate (APR), which incorporates both the interest charge and any lender fees. Even a distinction of one or a percentage point in APR can translate to masses — occasionally heaps — of greenbacks over the lives of a mortgage.

For example, on a $25,000 loan over 60 months:

- At 5% APR, you pay around $3,307 in overall interest

- At 8% APR, you pay round $five,496 in total hobby

That $2,000+ difference doesn’t come from the car — it comes from the loan. selecting subjects accurately.

Check your credit score first

Your credit rating is the single largest factor lenders use to determine your interest rate. The better your rating, the lower the rate you will qualify for. Typically speaking:

- 750+ — tremendous charges, exceptional loan terms

- seven-hundred–749 — correct fees, most creditors will compete for your commercial enterprise

- 650–699 — truthful fees, but room for negotiation

- underneath 650 — better quotes; don’t forget improving your rating earlier than applying

Pull your credit report before applying for any mortgage. search for mistakes or old information that is probably dragging your score down — disputing these can bring about a quick development. If your score wishes paintings, even ready three to six months to pay down current debt can meaningfully decrease the rate you obtain.

Keep more than one lender — not simply the Dealership

One of the most unusual mistakes vehicle buyers make is accepting the supplier’s financing provided without assessing their purchasing. dealers do offer convenience, and once in a while, manufacturers run promotional rates; however, they also have room to mark up the hobby fee — pocketing the distinction as earnings.

Before visiting a dealership, get pre-approved by using at least two or 3 lenders:

- Banks — Your existing financial institution may offer loyalty reductions

- credit unions — frequently provide the most competitive costs and flexible phrases

- online creditors — rapid approvals and clean credit equipment

- manufacturer financing — Can consist of zero% APR promotional deals, but requires robust credit

Getting pre-approved doesn’t hurt your credit score if you do it inside a brief window (generally 14–45 days, depending on the scoring version). Multiple applications in this era are counted as a single inquiry.

When you walk right into a dealership with a pre-approval in hand, you are negotiating from a position of energy.

Select the right loan term

Mortgage terms normally vary from 24 to eighty four months. Shorter phrases suggest higher month-to-month payments; however, less total interest paid. Longer terms lower your monthly price but value significantly more over the years.

Right here’s the trade-off in simple phrases: a 72-month mortgage might seem less difficult month to month, however, you’re paying interest for two extra years as compared to a forty eight-month mortgage. You’re additionally much more likely to be “underwater” — owing more than the car is worth — for longer, which creates issues if you need to promote or if the car is totaled.

As a preferred guiding principle:

- New motors: intention for forty eight–60 months most

- Used automobiles: intended for 36–forty-eight months

In case you cannot manage to pay for the monthly payments on a shorter-term mortgage, it is generally a sign that the automobile price is beyond your finances, not a motive to stretch the time period.

Factor within the Down fee

A larger down payment reduces the amount you borrow, which lowers both your monthly payment and your total cost. It also reduces the hazard of going underwater on the mortgage.

Most financial advisors recommend placing down as a minimum of 10–20% of the car’s purchase price. On a $30,000 vehicle, this is $3,000 to $6,000 prematurely.

When you have a trade-in car, its cost can function as part of your down fee. Get impartial prices to your alternate-in earlier than the dealership makes an offer — knowing its marketplace cost prevents you from being lowball.

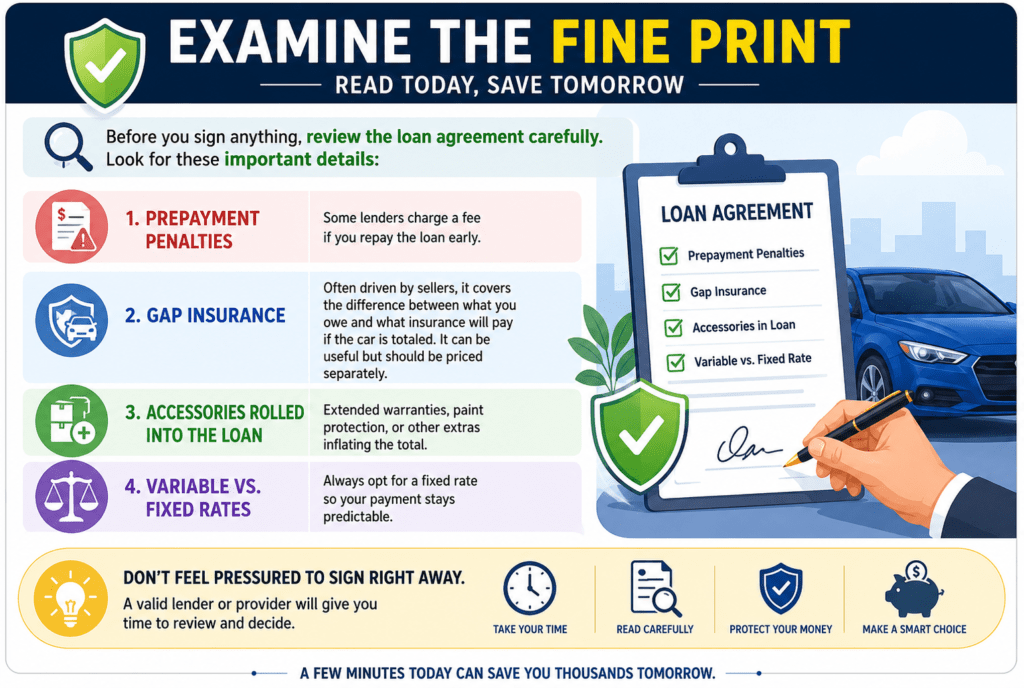

Examine the nice Print

Before you sign something, evaluate the mortgage agreement carefully. watch for:

- Prepayment penalties — some lenders charge a fee if you repay the loan early

- hole insurance — frequently driven by using sellers, it covers the difference between what you owe and what insurance will pay if the auto is totaled; it is able to be useful but should be priced one after the other

- accessories rolled into the loan — prolonged warranties, paint safety, or other extras, inflating the essential

- Variable vs. fixed quotes — continually opt for a hard and fast charge so your price stays predictable

Don’t sense compelled to signal instantaneously. A valid lender or provider will give you time to check.

Conclusion

The quality car loan isn’t the only one with the flashiest ad or the lowest monthly payment — it’s the one that fits your real financial picture. understand your budget, test your credit score, compare multiple lenders, keep the term affordable, and examine every line before you sign. Taking some extra hours to do your homework can effortlessly prevent lots of bucks and years of financial stress.

An automobile needs to open doors for you, not close them.