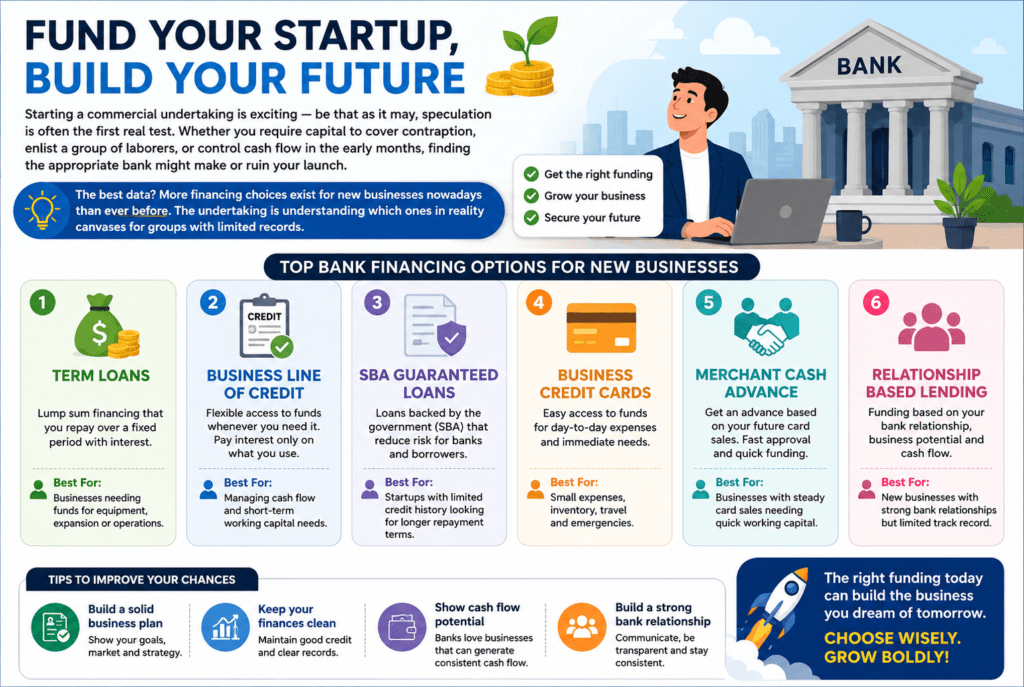

Starting a commercial undertaking is exciting — be that as it may, speculation is often the first real test. Whether you require capital to cover contraption, enlist a group of laborers, or control cash flow in the early months, finding the appropriate bank might make or ruin your launch. The best data? More financing choices exist for new businesses nowadays than ever before. The undertaking is understanding which ones in reality canvases for groups with limited records.

Why Startup Loaning Is one of a kind

Most ordinary banks require at least two years of running history, and some recently favor a commercial venture contract. For a logo-new undertaking, that’s a dealbreaker. New companies, too, tend to have lean credit score profiles, unusual income, and confined collateral — all of which make conventional banks cautious.

It is why startup authors need to appear past the colossal banks and investigate lenders particularly planned to serve early-stage businesses. The choices range from SBA bundles to online fintech loan specialists, each with particular preferences depending on your timeline, credit score, and financing needs.

SBA Credits — charming for long-time period, Low-cost Financing

The U.S. Small Business Administration (SBA) doesn’t loan cash specifically — it ensures credits issued by accredited lenders, bringing down the chance for banks and making it less difficult for new businesses to qualify. The

SBA 7(a) contract is the most popular program. It covers a broad assortment of employments which include running capital, equipment, and real estate. credit amounts can pass up to $five million, and side interest costs are commonly lower than most extreme online moneylenders. The tradeoff is time — SBA advances include more printed material and longer endorsement timelines.

SBA Microloans are tailor-made for early-stage and underserved organizations. contract wholes cross as much as $50,000, making them ideal for modern businesses that require a modest capital mixture to get off the ground. charges tend to be sensible, and nonprofit mediators frequently offer commercial venture help near the funding.

excellent for: New companies with at least three hundred and sixty-five days of operation, a strong promotional methodology, and the ability to explore an exhaustive utility process.

Progress Capital — remarkable for adaptable Startup strains of credit

Headway Capital always positions a few of the apex startup-friendly moneylenders for one clean reason: it requires six months in commerce to qualify, one of the shortest terms of any moneylender in this course. For marketers who’ve fairly gotten off the floor, it genuinely is a full-size advantage.

Headway offers a spinning line of credit with a score up to $100,000 with terms beginning from 12 to 24 months. The negligible yearly deals necessity is $50,000 (kind of $4,167 steady with month), which is intentioned moo in comparison to comparable competition. There are no prepayment punishments, and funds can be accessible on the subsequent commercial undertaking day after approval.

It’s well worth noticing that Headway’s flexible repayment shape works pleasantly for offices with conflicting early income — a common truth for new companies still developing their supporter base.

pleasant for: Unused businesses (6+ months collectible) that require open, rotating credit score without strict deal thresholds.

Lendio — first-rate showcase for Startup contract buying

as contradicted to a single moneylender, Lendio is a advance commercial center that interfaces indebted individuals with over seventy-five lenders, which include the USA, OnDeck Capital, and speculation Circle. This gives new companies the potential to compare more than one offer in a single locale, rather than applying to banks individually.

Lendio is one of the few marketplaces that offer startup advances in specific, with amounts fulfilling as much as $10 million and terms of as much as five years at forceful costs. The platform’s tremendous community implies originators with unmistakable credit profiles and trade sorts can find a fit more effectively than through a single organization.

The computer program preparation is streamlined, and numerous indebted individuals get hold of speculation gives interior 24 hours of applying.

nice for: New companies that require looking at a couple of contract stocks fast and discover the most compelling rate without different troublesome credit score pulls.

Taycor Financial — fine for gear and Resource Financing

If your startup wishes for apparatus, engines, or era to work, Taycor Financial is a standout choice. It makes a forte of hardware financing for more up-to-date businesses and gives advances from as little as $500 as much as $five million, with venture practical in as little as one business day.

Taycor works with a range of credit profiles and is broadly open to groups that are still in their early stages. The viewpoint charge form (extending from 1.10 to at least one 36) strategy charges are self-evident, in spite of the fact that it is worth doing the arithmetic to compare the successful APR with other alternatives.

first-class for: New businesses in generation, coordination, healthcare, or any venture in which physical infrastructure is crucial to operations.

Fundbox — extraordinary for prompt access to working capital

Fundbox gives a commercial venture line of credit beginning at 4. sixty six% intrigued, with speculation to be had as early as the consequent venture day. It’s planned for companies that need expedient get affirmation to coins to cover quick-term holes — finance, stock, or a slow-paying consumer.

The endorsement strategy is direct, with negligible documentation required. Fundbox employs real-time commercial undertaking realities (bank account activity, bookkeeping program integration) to evaluate financial soundness, which is particularly advantageous for new companies that do not have a long history of financial statements to reveal.

satisfactory for: New businesses with enthusiastic cash flow that need a brief, low-friction line of credit.

Bluevine — palatable for building a commercial endeavor credit

Bluevine offers lines of credit up to $200,000 with a least credit rating of 625. one in each of its key advantages for new companies is that it reports to trade credit bureaus, which implies each on-time installment effectively builds your trade credit score profile. For a brand modern commercial venture, that long-term advantage is basically as prized as the capital itself.

Bluevine can finance up to 12 to 24 hours of endorsement, making it one of the speedier choices among snared up online banks. The least intrigued cost begins at 14%, which is competitive for a non-collateral line of credit, in spite of the fact that week after week reimbursements are required.

Notice: Bluevine isn’t accessible in North Dakota, South Dakota, or Nevada.

first-rate for: New companies looking to get right of section to capital and at the same time build a solid endeavor credit history for future financing.

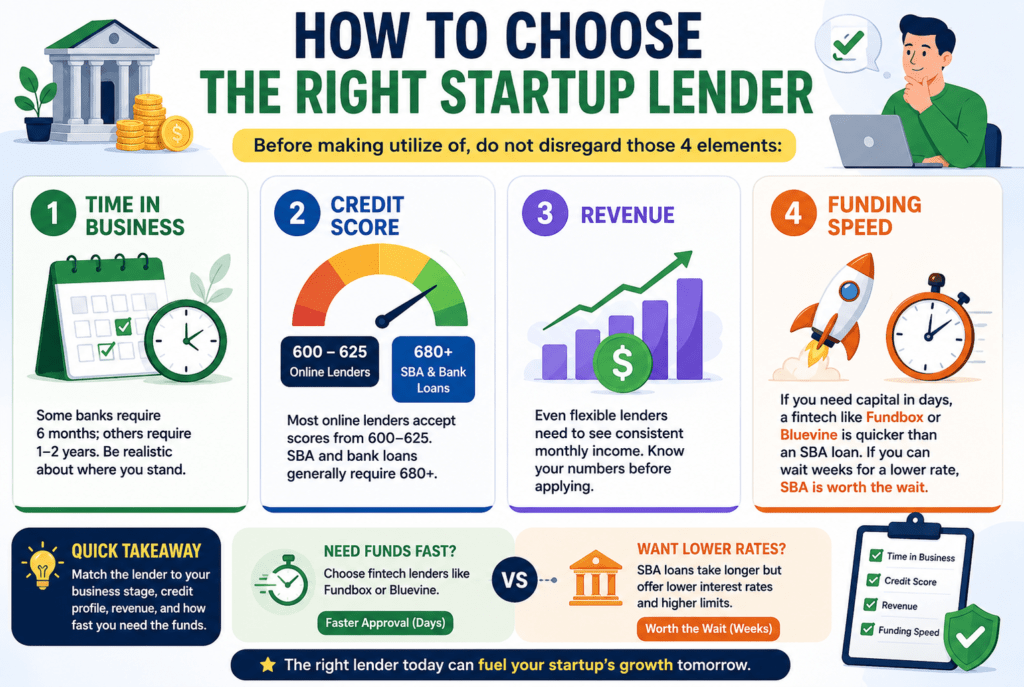

How to choose the right Startup Lender

before making use of it, do not disregard those 4 elements:

- Time for undertaking. A few banks require 6 months; others require 1–2 years. Be sensible about where you stand.

- credit score. Most online lenders give evaluations from six hundred 625. SBA and monetary institution credits for the most part require 680+.

- revenue. Indeed, flexible loan specialists require a consistent month-to-month wage. know your numbers before making use of.

- investment pace. If you need capital in days, a fintech like Fundbox or Bluevine is quicker than an SBA contract. If you can hold up weeks for a diminished charge, SBA is truly worth the wait.

Conclusion

There may be no single quality loan specialist for each startup — the appropriate inclination depends on how long you have been working, what you require the funds for, and how quickly you require them. What’s greatest is applying to moneylenders whose prerequisites certainly suit your modern-day situation, as opposed to investing time on programs you’re not likely to bypass.

begin with the choices that in shape your profile, look at terms cautiously, and do not disregard the perspective on the long-term value of borrowing, not the credit amount you get.