Banking must be just right for you — not towards you. Yet thousands and thousands of humans lose hundreds of dollars every year to expenses they in no way saw coming: Maintenance fees that quietly drain checking accounts, ATM surcharges that stack up on avenue trips, Overdraft consequences that hit hardest when cash is already tight. The frustrating truth is that a lot of these fees are completely avoidable as soon as wherein to appearance and what to do.

Here is a practical, no-fluff manual for identifying hidden financial institution fees and making sure you prevent paying them.

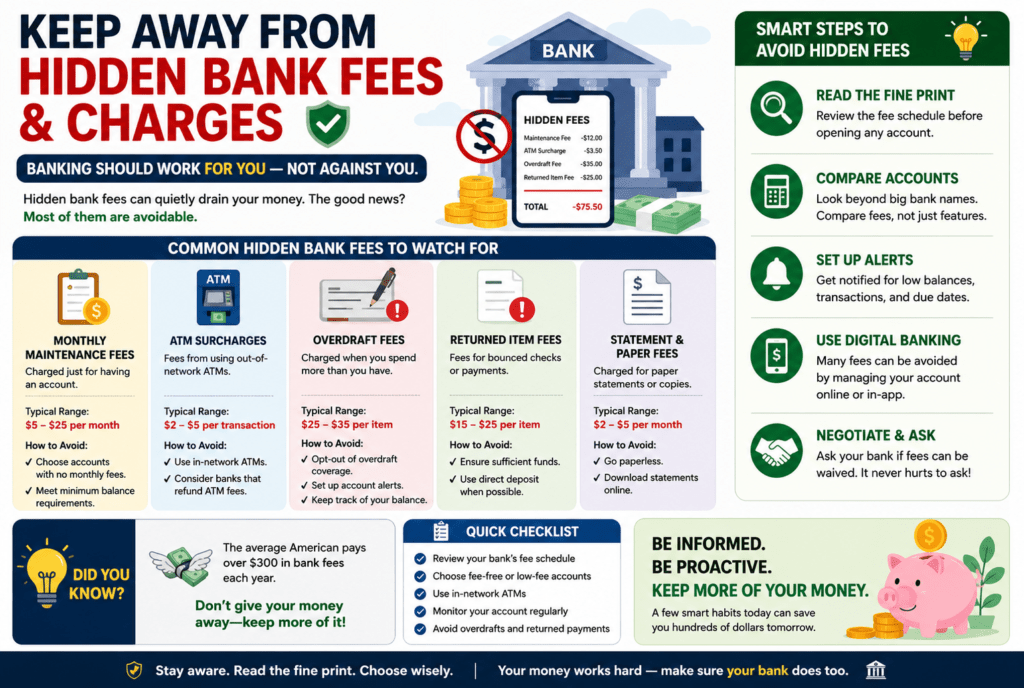

Apprehend the maximum common Hidden bank charges

Earlier than you can avoid fees, you need to know which of them exist. Banks are required to disclose their price schedules, but they hardly ever put them on the market themselves. The most unusual expenses purchasers overlook include:

- Monthly protection prices — many conventional banks price $10–$25 in step with month for having a checking or savings account. These expenses are frequently avoidable if you meet sure situations, but banks count on clients not knowing that.

- Overdraft and Non-Sufficient Funds (NSF) costs — that is one of the most highly-priced traps. While your account stability falls short, banks normally charge $25–$38 in keeping with transaction. A few banks even price a couple of overdraft prices in a unmarried day.

- Out-of-network ATM costs — the use of an ATM outside your bank’s network can bring about a double rate: one from your very own financial institution and one from the ATM owner. Together, these can effortlessly upload as much as $5–$8 in keeping with each withdrawal.

- Minimal balance charges — some bills require you to hold a minimal balance every day or month-to-month. Failing below that threshold, even as soon as, a charge is brought on.

- Paper declaration fees — Banks increasingly price $1–$five consistent with the month if you get paper statements in place of opting into e-statements.

- wire switch and overseas Transaction expenses — Sending money regionally or across the world often incorporates costs starting from $15 to $50 in keeping with transfer. Foreign transaction costs usually add 1–3% on top of every buy made overseas.

- Inactivity fees — leave an account dormant for too long without any transactions, and a few banks will charge you a month-to-month inactivity fee.

Examine Your Account settlement and fee timetable

This step sounds tedious; however, it is one of the most powerful things you could do. While you open a bank account, you acquire a deposit agreement and a price disclosure report. The majority forget about both.

Take thirty mins to read via the price timetable. Appearance specifically for:

- What triggers each fee?

- What situations permit a charge to be waived,

- whether prices have been modified these days (banks are allowed to replace their fee systems with notes)

If you already have an account and have in no way read those files, Log in to your online banking portal and download the current fee agenda. Banks are legally required to maintain these records handy. Knowing exactly what you are being charged — and why — places you in control.

Meet Waiver requirements or transfer Account sorts

Many monthly protection charges may be waived without a doubt with the aid of meeting one of the numerous conditions. Common waiver qualifications consist of:

- Putting in a qualifying direct deposit every month

- Keeping a minimal common balance each day

- Creating a minimum variety of debit card transactions consistent with the declaration cycle

- Being a pupil, senior, or army member

In case your bank offers a rate waiver and you aren’t taking advantage of it, contact customer service and find out exactly what you need to do. In many cases, routing your paycheck immediately to your bank account is all it takes to take away a $12–$15 monthly charge completely.

If the waiver situations are definitely difficult to satisfy, given your monetary situation, bear in mind switching to a special account tier. Most banks offer basic or scholar loans with lower or no costs.

Choose Out of Overdraft protection (Strategically)

This one surprises many humans. Banks normally sign up customers in overdraft safety by default, which sounds beneficial — your transaction is going through even when finances are inadequate. However, the cost is steep: an unmarried $35 overdraft fee on a $5 coffee purchase isn’t safe, it’s miles a penalty.

You have the legal right in most nations to opt out of overdraft coverage for debit card transactions. While you do, the transaction is in reality declined at the point of sale in preference to going through and triggering a fee. Whilst a declined card may be inconvenient, it’s far, far less damaging than stacking overdraft charges.

Alternatively, hyperlink your checking account to a financial savings account as an overdraft buffer. Many banks allow transfers from financial savings to cover shortfalls, frequently with a much smaller switch charge, or no charge at all.

Use In-community ATMs and virtual options

Get acquainted with your bank’s ATM community and stick with it. Most banks and credit score unions post ATM locator equipment on their apps. Earlier than journeying, discover in-community ATMs at your vacation spot to keep away from wonder fees.

Higher yet, use digital fee strategies — debit cards, mobile wallets, and peer-to-peer apps — to lessen your reliance on cash altogether. When you do want cash, consider making money again at grocery or convenience shops during a debit card buy. That is typically unfastened and saves you an ATM experience entirely.

In case you often travel the world over, investigate money owed in particular designed for travelers. Several online banks and credit unions offer 0 overseas transaction charges and even reimburse ATM surcharges globally.

Recall online banks and credit Unions

Traditional brick-and-mortar banks deliver the best overhead expenses, and people costs are frequently passed on to clients through prices. Online banks operate with much lower fees and routinely provide accounts without a monthly maintenance cost, no minimum balance requirements, and no overdraft fees.

Credit unions are a wonderful opportunity. As member-owned, not-for-profit institutions, credit score unions usually charge substantially lower expenses than commercial banks and offer better interest rates on both deposits and loans. Club eligibility varies, but many credit score unions have broadened their criteria and are available to a maximum number of consumers.

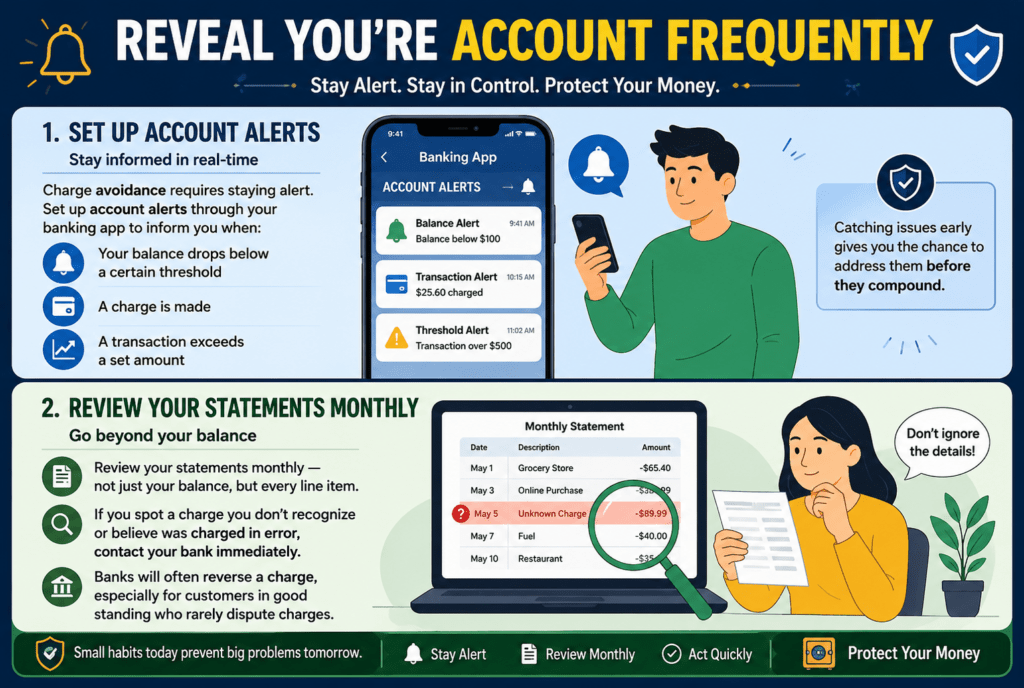

Reveal You’re Account frequently

Charge avoidance requires staying alert. Set up account alerts thru your banking app to inform you when your balance drops below a certain threshold, when a price is charged, or when a transaction exceeds a hard and fast amount. Catching issues early gives you the danger to address them earlier than they compound.

Review your statements monthly — now not just your stability, but also each line item. If you spot a rate you do not recognize or agree with changed into charged in mistakes, call your financial institution without delay. Banks will regularly charge a price, especially for customers in a true status who rarely incur costs.

Negotiate and propose for yourself

Banks want to preserve customers. If you have been with your financial institution for years and have, in any other case, maintained your account in its exact status, you have greater leverage than you suspect. A well-mannered name to customer support soliciting for a fee to be reversed is often exceptionally powerful.

If your bank is always charging costs you cannot keep away from, that could be a signal to keep around. Loyalty to a financial institution that does not serve your economic interests costs you cash each month. Evaluate accounts, study reviews, and make the move if a better option exists.

Hidden bank prices are not inevitable — they may be a system that works handiest whilst clients remain uninformed. With a touch of consciousness and a few planned actions, you can maintain appreciably more of your very own money where it belongs: for your account.