The conventional preserving money shape — constructed on real branches. Lengthy workplace work and layers of fees are confronting its finest mission. A brand new generation of fintech organizations is revamping the direction of funding. Putting satisfactory decrease back into the hands of shoppers and businesses alike. Fueled by the assistance of synthetic insights, cloud-based, and mobile-first layout. These businesses aren’t basically competing with banks — they’re converting them.

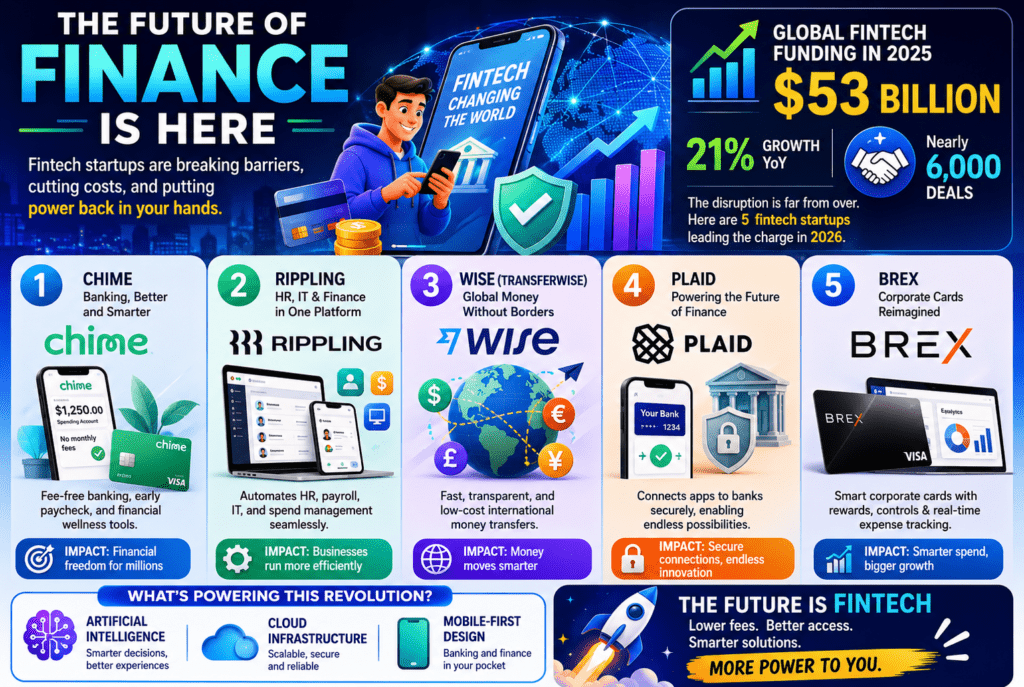

worldwide fintech subsidies rose via means of 21% in 2025. Carrying out $ fifty-three billion in the course of nearly 6,000 deals, a clear signal that the disturbance is far from over. proper right here are 5 fintech new groups essential for the cost in 2026.

Revolut — The All-in-One monetary momentous App

Few fintech organizations have advanced as forcefully or as strikingly as Revolut. set up in London in 2015. Revolut started as a simple money replacement tool and has, considering. The fact that it stepped forward into one of the most general financial levels in the industry.

group profits hit $6 billion in 2025, up 46% 12 months over twelve months. Driven by a massive component of endeavor keeping cash administrations. Revolut also published a gain some time recently, a charge of $2.three billion, and came to kind of sixty-nine million retail and assignment clients. To position that amid point, several customary mid-sized banks have taken a long time to construct similar supporter bases.

What sets Revolut apart is its breadth. Clients can oversee payments. Cash-related funding, speculations, cryptocurrency, or certainly scope — all from a single app. The employer works in forty nations and received a complete U.okay. preserving cash permit in 2026, a first-rate administrative leap forward that. Brings it toward becoming a fully authorized global financial organization.

Revolut raised $2 billion at a $75 billion valuation, making it the most prized non-public neobank of all time. With ambitions to hit 100 million clients by 2027, Revolut is presently no longer a challenger — it is distant from being a cutting-edge brand.

Nubank — handling an account for the Underserved at massive Scale

Nubank has approved that the maximum feasible disturbance regularly takes place where everyday banks have fizzled the most severe. Based in Brazil in 2013, Nubank set out to serve the hundreds of thousands of Latin Americans who have been unbanked or caught in high-price, low-service preserving money relationships.

In recent times, Nubank has over a hundred million clients across Latin America and is effectively pushing into modern markets. Which include making use of a U.S. savings account. Its shape is developed on effortlessness: no physical branches, no hidden charges. And a totally computerized experience that can be established in mins from a smartphone. CPOstrategy

The financial comes approximately communicate for them. Thru efficaciously pass-promoting credit cards and character advances to its enormous consumer base in Brazil, Mexico. And Colombia, Nubank produced almost $2 billion in internet pay in 2024. That stage of productivity is unusual amongst neobanks, and it comes from profound information about its patron base.

Nubank produces maximum people of its deals — sort of 70 to 85 percent — from intrigued benefits on credit score rating cards. Personal advances, and related objects, a display that makes sticky, repeating earnings input of depending totally on trade charges. Because it eyes U.S. expansion, Nubank may additionally want to become the first of all in reality worldwide emerging-market neobank.

Chime — Reclassifying purchasers retaining cash inside the U.S.

In a world where overdraft prices on my own fee human beings billions of bucks every 12 months, Chime constructed its entire persona circular, doing away with them. Founded in 2012 and based in San Francisco, Chime has become the best purchaser neobank in the USA.

Chime emphasizes no-rate retaining cash and early coordinate save get section to. Scaling to billions in offers with moving ahead benefit through compatibility and later credit score rating inventory. Its center assurance is radical in its straightforwardness: no month-to-month fees, no negligible equalizations, and get to your paycheck up to 2 days early. Crowdfund Insider

Chime wrapped up the biggest-ever U.S. neobank IPO with its $864 million open advertising and marketing in June 2025, a point of reference that showed the neobank exhibit for corporation speculators and signaled that digital-first preserving cash is no longer a hollow lesson — it is distant mainstream.

Chime’s purchaser base skews in the direction of extra youthful, paycheck-to-paycheck individuals who’ve been sincerely underserved by traditional banks. by implies of, get them collectively, wherein they’re — on their telephones, without the terrorizing of office visits or credit score appraisals — Chime has constructed furious devotion amongst a statistic that occupants have long neglected.

Stripe — the Framework inside the back of the automated economic gadget

While the maximum severe fintech disruptors compete quickly with consumer banks, Stripe works one layer more profoundly — and seemingly with a certainly more distinguished effect. Primarily based in 2010 thru brothers Patrick and John Collison, Stripe manages the installment basis that powers millions of companies worldwide.

Stripe partners with crucial groups and celebrated manufacturers, including Portage Engine trade undertaking and Spotify, displaying value handling pc software, interfacing for e-exchange systems, and complicated bookkeeping apparatuses. In rapid, if an undertaking recognizes coins online, there may be an exquisite peril. Stripe is worried about some vicinity in that machine.

What makes Stripe definitely difficult to maintain cash is its function within the implanted fund insurgency? The agencies on the 2026 Forbes Fintech 50 are not truthful in building customer apps. They’re making the innovation basis that powers modern-day economic structures. From installment structures and character affirmation systems to implanted back units. Stripe is at the center of this pass, empowering any trade challenge to emerge as money related administrations enterprise while not having a money license.

With a valuation of $ ninety-one. Five billion and increasing items in alternate lending, corporate cards, and income financing, Stripe is discreetly developing an economic area that sits under the overall virtual economy.

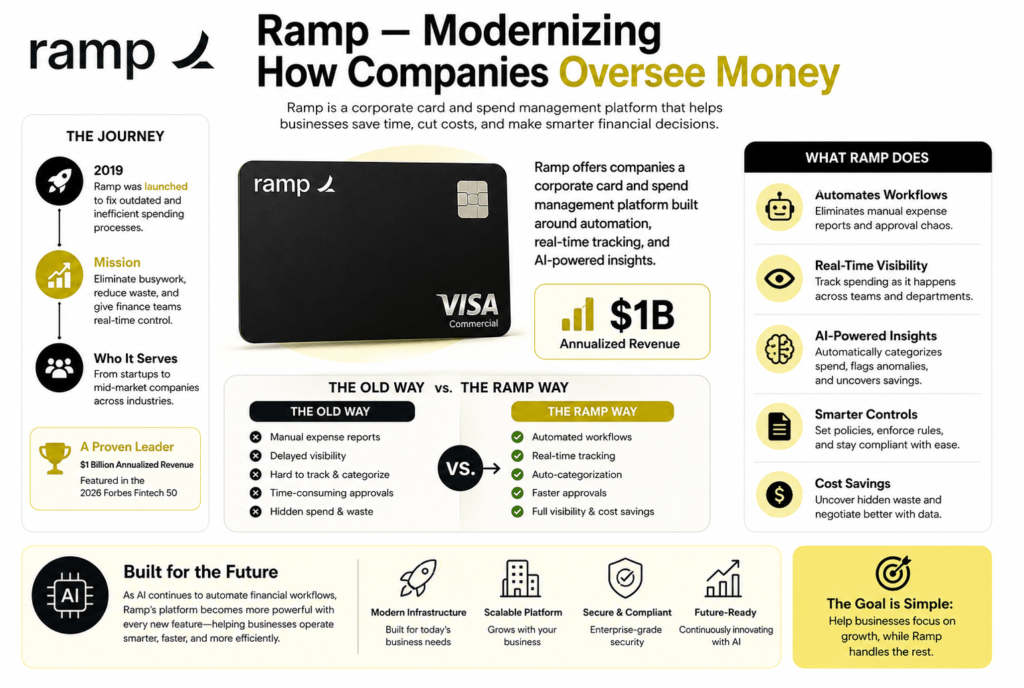

Incline — modernizing how groups oversee money

The company has again been moderate, direct, and frugal with wastefulness. Incline changed into hooked up to reestablish that. Discharged in 2019, Incline offers companies a company card and spend administration degree, built on circular computerization, real-time fetched checking, and AI-powered insights.

Ramp is a corporate credit score rating card startup with annualized earnings of $1 billion, a greatly extraordinary victory for a commerce task less than a decade old. Its pitch to groups is apparent: halt dropping time on fetched reviews and permit application software to oversee it. Slope automatically categorizes making an investment, banners unheard of fees, and produces cash-related reserve price range insights — tasks that already required total fund groups.

The 2026 Forbes Fintech 50 reflects an endeavor to replace within the route of foundation. Business enterprise structures, and low-priced commerce fashions, and Slope is a sure culmination of this slant. Instead of specializing in shoppers, it goes after the undiscovered wastefulness inside places of work — from new agencies to mid-market agencies. And replaces their legacy retaining money hardware with something quicker and smarter.

As AI continues to robotize economic workflows, Ramp’s reveal will end up more capable with every unused highlight it ships.

Conclusion

The disturbance of traditional handling of accounts is not a future event — it’s miles as of now occurring. The process of putting it on the market is solidifying right into a barbell form, overwhelmed by means of expansive occupants and massive neobanks. Crushing out mid-sized territorial banks. Revolut, Nubank, Chime, Stripe, and Slope each speak to a specific aspect of this modification. Universal exquisite apps, money associated incorporation at scale, charge-free benefactor retaining money, fee foundation, and AI-driven change finance.

For shoppers and bunches alike, the message is clear — you presently have additional choices than ever a while currently. And individuals’ choices have become much higher each year.