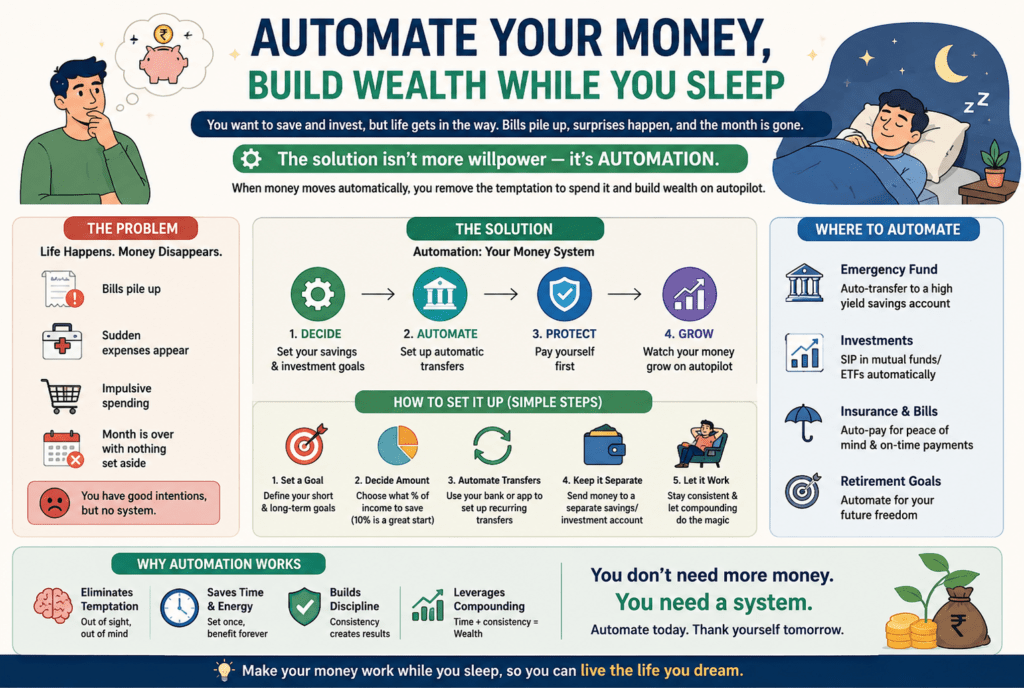

. The general public understands they have to keep and invest, but existence gets in the way. bills pile up, sudden expenses appear, and before you realize it, the month is over with nothing set aside. The reply is not an additional region — it is automation. Whilst cash movements are routine, you dispose of the temptation to spend it and build wealth on autopilot.

Here is everything you need to recognise approximately putting in place a machine that works even as you sleep.

Why Automation Works

Human psychology isn’t stressed out by constant economic behaviour. We reply to what is in front of people, and if money is sitting in a checking account, it feels to be spent. Automation solves this by making saving the default, not the exception.

Research continuously displays that individuals who automate their savings gather greater wealth over the years — not because they earn extra, but due to the fact that they never put themselves the threat to spend what they planned to shop. The “pay yourself first” philosophy has been the spine of personal finance recommendations for decades, and automation is honestly the current device to execute it without effort.

Audit your current cash flow

Before you automate anything, you want a clean picture of your price range. Study your final three months of bank statements and pick out your common monthly income after tax, your fixed expenses (hire, utilities, loan bills), your variable charges (groceries, dining, leisure), and what sort of is generally left over by month.

This exercise exhibits your real saving capacity, which is often different from what humans estimate. Even assuming the amount shows up a little, it’s distant enough to start.

Open the right accounts

Automation requires the proper account infrastructure. At minimal, you have to have a dedicated financial savings account separate from your normal checking account. The physical separation creates a psychological barrier that reduces the urge to dip into financial savings.

For investing, do not forget to open a brokerage account or, if available in your state, a tax-advantaged account along with a retirement fund or personal savings account. Many structures today provide commission-free investing and let you start with minimal amounts.

Pick debts with no or low monthly charges and, for savings, search for the very best interest rate available. high-yield savings money owed can earn extensively more than widespread debts, making them perfect for quick and medium-time period goals.

Set up automatic Transfers for savings

As soon as your bills are in vicinity, schedule a habitual computerized switch out of your bank account to your financial savings account. The most effective timing is the day after your salary arrives — this guarantees money is moved earlier than discretionary spending starts offevolved.

Begin with a practical amount. If you can have the funds to store 10% of your profits, start there. If that feels too aggressive, start with three% or 5% and grow it each few months. The secret is constructing the habit first and scaling later.

Most banks will let you set those exchanges quickly thru their cell app or online portal. Call your savings account after your intention — “Emergency Fund,” “travel 2026,” “house Deposit” — to make the reason feel concrete and motivating.

Automate Your Investments

Saving cash is step one; growing it is step. Funding automation guarantees your money is continuously working for you instead of sitting idle.

The best approach for the general public is dollar-price averaging, which means investing a hard and fast quantity at regular intervals regardless of market conditions. Whilst expenses are high, your fixed quantity buys fewer devices. While prices are low, it buys more. Over the years, this has smoothed out marketplace volatility and eliminated the anxiety of looking to time the marketplace.

Most brokerage platforms and investment apps will let you install a routine investment contribution. You could direct these into an index budget, exchange-traded funds (ETFs), or other diverse assets relying on your risk tolerance and funding goals. Index funds in particular are a popular choice for computerized investing because of their low fees and huge market exposure.

For retirement-specific debts, many employers offer payroll deductions that automatically direct a percentage of your profits into a retirement fund before it even hits your bank account. In case your company gives matching contributions, take full advantage — it’s miles efficaciously loose cash.

Automate bill payments

At the same time, now not without delay, a savings method, automating your bill payments, gets rid of late fees and protects your credit score. Set all fixed monthly prices — utilities, subscriptions, mortgage repayments — to autopay. This additionally gives you a purer view of your authentic discretionary spending every month.

Be cautious with subscriptions. Automate only what you actively use and audit your subscriptions every six months to cancel services you have forgotten about.

Use Round-Up and Cashback capabilities

Numerous banking apps and systems offer round-up features that round each buy to the closest dollar and convert the difference into savings or investments. At the same time, as the number of men or woman quantities are small, the cumulative effect over months adds up meaningfully and builds the dependency passively.

Some credit and debit cards also offer cashback rewards that may be redirected automatically right into a savings or investment account. In case you have already spent money, having an element return to you and compound in an investment account is a low-risk wealth-building method.

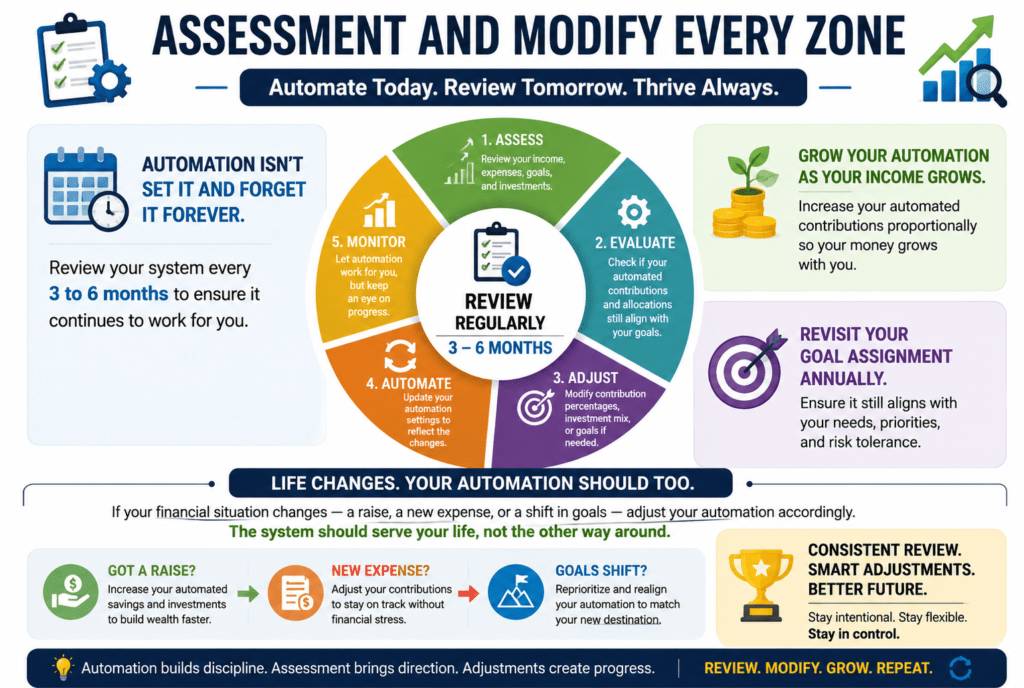

Assess and modify every zone

Automation does not suggest set it and forget about it forever. Overview your gadget every 3 to six months. As your income grows, increase your automated contributions proportionally. Revisit your speculation assignment annually to guarantee it, in any case, aligns with your wants and risk appetite.

In case your monetary situation adjustments — a boost, a new expense, or a shift in goals — regulate your automation for this reason. The machine should serve your lifestyles, not the alternative manner around.

The Compound impact of beginning Early

The most powerful aspect of computerized saving and making an investment is time. Cash invested over a long duration always grows exponentially due to compound interest. Even modest monthly contributions can develop into enormous wealth over a decade or more. The high-quality time to begin changed into the day gone by. The second-best time is today.

Automation eliminates the friction, emotion, and forgetfulness that derail maximum monetary plans. Set it up as soon as, overview it on occasion, and permit your monetary future build itself within history.

/