For millions of Americans, Social Security is the backbone of retirement income. However, right here’s what the general public does not recognise: the quantity you receive isn’t always set in stone. The choices you are making — when to assert, how long to paint, and how to coordinate advantages with a spouse. Can dramatically grow or lower your monthly take-home pay for the relaxation of your existence. With the appropriate methodology, you may collect tens of thousands of greenbacks additional over your retirement years. Here’s exactly the way to make that manifest.

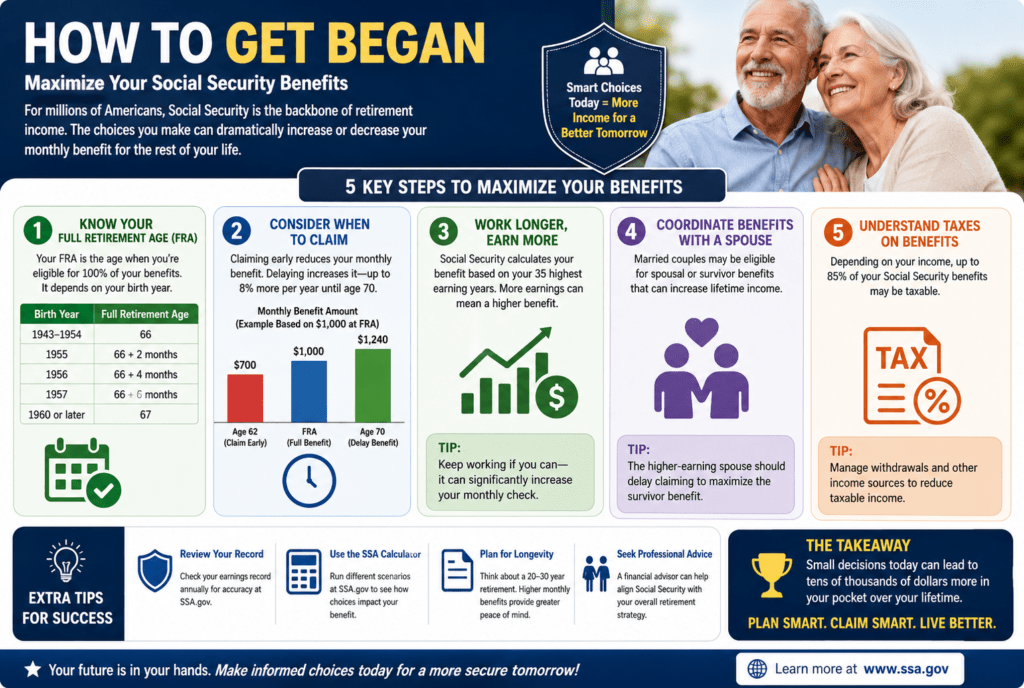

Apprehend How Your advantage Is Calculated

earlier than you can maximize Social safety, you need to recognize what drives your benefit quantity. The Social Security Administration (SSA) examines your lifetime earnings history. And indexes your maximum 35 years of earnings to decide your monthly benefit. This parent is referred to as your common listed monthly earnings (AIME), and it includes the sum of the whole lot you may receive.

If you labored fewer than 35 years, the SSA fills in the missing years with zeros. Which lowers your average considerably. That by itself is an effective cause to preserve operating, even part-time, if you’re drawing close to retirement with gaps in your work records.

Work at least 35 Years — and earn more when you can

profits on the report. Running for at the least 35 years with a higher income without delay increases your gain calculation. In case you’re nonetheless operating, and your current earnings are higher than what you earned in previous years. Continuing to work replaces the lower-earning years in the SSA’s method — bumping up your common and, consequently, your monthly gain.

In 2026, the maximum taxable income cap rose to $184,500. Which means wages as much as that quantity are credited towards your Social Security record. When you have the ability to grow your profits — via promotions, aspect income, or self-employment — now’s the time to do it.

Postpone Claiming for an assured 8% Annual enhance

That is the single maximum effective lever available to maximum retirees. In case you postpone taking your benefits, your monthly check will increase for each month you wait, until age 70. With an additional 2/3 of one percent for every month you postpone after your full retirement age (FRA), including up to eight percent for each complete 12 months you wait.

You can begin retirement benefits as early as sixty-two; your monthly benefit is completely decreased if you claim earlier than your complete Retirement Age. For the ones born in 1960 or later, FRA is sixty-seven.

Delaying advantages until age 70 can increase your monthly payments with the aid of 24% compared to. Claiming at the complete retirement age of sixty-seven. Think about what meaning over a long retirement: if you live to eighty five, the difference between claiming at sixty two as opposed to 70 is $sixty six,240 in total lifetime benefits. If you live to 90, the hole develops to $137,280.

The 8% annual increase from behind-schedule retirement credits is considered the nice, assured, inflation-adjusted return available in any monetary product. There is one firm rule to bear in mind: in no scenario should you put off advantages beyond age 70. As this is while behind schedule retirement credit prevents amassing.

Understand the income limit in case you declare Early

Many people do not recognise that if you declare advantages before your FRA and keep running. Your benefits can be briefly decreased. If you haven’t reached your full retirement age, $1 in benefits might be deducted for each $2. You earn above the yearly earnings limit ($24,480 in 2026). inside the 12 months you reach your complete retirement age. The discount falls to $1 for each $three you earn above a better restriction ($65,160 in 2026). But once you hit your FRA, your advantages are no longer decreased, irrespective of how much you earn.

The best information: the SSA will recalculate your Social Security payments to consist of the deducted amounts. Resulting in better benefits going ahead. But it’s still really worth planning cautiously in case you intend to continue working after claiming early.

Leverage Spousal and Survivor advantages

In case you’re married, you and your partner have large planning possibilities that can meaningfully increase your family’s overall Social Safety Income. Spousal and survivor advantages can provide up to a hundred percent of the higher earner’s benefit when deliberate strategically.

In general, a partner who earned much less in the course of their career can declare up to 50% of the higher earner’s FRA gain. the smartest method for lots couples is to have the lower earner claim early. Even as the better earner delays till 70, locking in the biggest possible base gain. This will become the survivor’s benefit if the better earner passes away first.

One crucial caveat: delaying advantages would not increase spousal blessings or the family’s gain. Delayed retirement credits handiest observe in your own individual gain, so the calculation needs to take into account both spouses’ conditions.

Do not forget divorced spouses, both. In case you’re divorced and were married for as a minimum 10 years, you will be eligible for benefits based on your ex-partner’s file without affecting their advantages or those of their current spouse.

Minimize Taxes for your benefits

Many retirees are amazed to discover that their Social Security benefits are in part taxable. Up to eighty five% of your advantage can be problem to federal income tax depending on your “combined earnings” — your adjusted gross earnings. Plus a nontaxable hobby, plus half of your Social Security benefit.

With the aid of coordinating Social Security benefits with withdrawals from pensions. 401(k)s, and IRAs, retirees can create a bendy earnings method. For example, drawing down conventional IRA funds in the years before you declare Social Security can lower your taxable income in later years. Roth conversions during low-earnings years are another smart pass, as Roth withdrawals do not count towards your mixed profits calculation.

Presently, forty-one states do not tax Social Security benefits at all — a factor well worth considering when you have flexibility about in which you retire.

Evaluate your earnings file frequently

Mistakes on your Social safety profits file are extra commonplace than you’d suppose — and that they at once have an effect on your benefit amount. Create a loose account at SSA.gov and evaluate your earnings history annually. If you spot a year where your earnings are missing or wrong, you may report a correction request with helpful documentation.

This step costs nothing and takes just a few mins; however, catching even one miscalculated yr may add meaningful bucks to your monthly advantage.

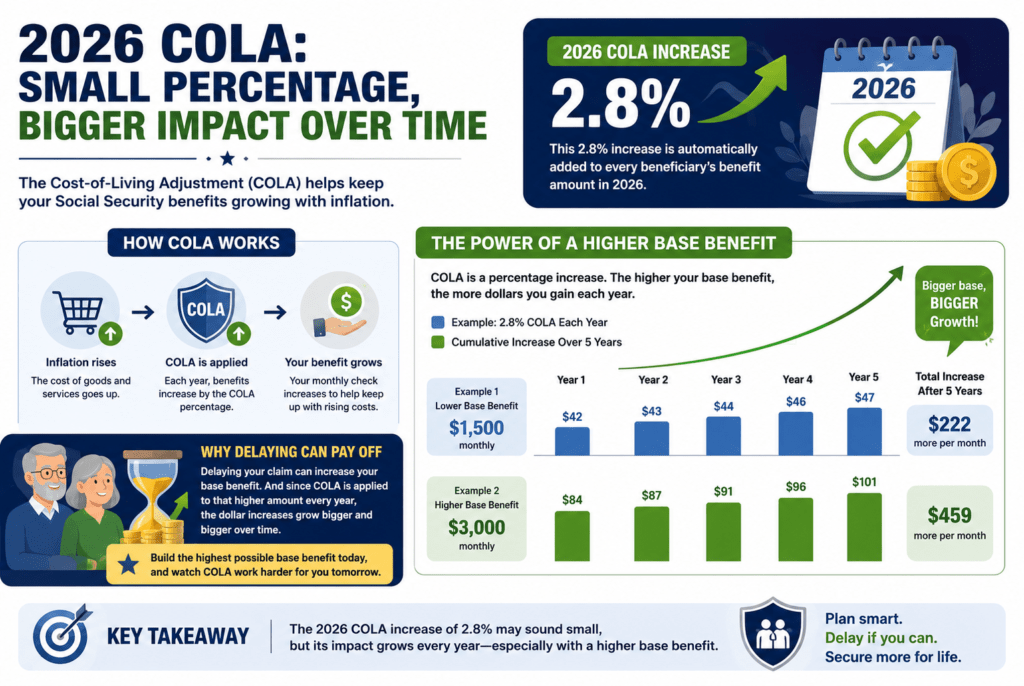

Keep in mind COLA

The 2026 value-of-residing Adjustment (COLA) increased through 2.eight%, automatically raising every beneficiary’s take-home pay. The higher your base benefit when you first declare. The larger each annual COLA growth might be in absolute dollar terms. This is every other reason why delaying and building the largest feasible base gain can pay off an increasing number of as the years pass.

Conclusion

Maximizing your Social safety advantages isn’t a unmarried choice — it’s a strategy built from more than one clever choice. Working long enough, earning as an awful lot as you can, delaying claims when financially feasible. Coordinating with your spouse and dealing with taxes successfully. The average Social protection advantage in 2026 is $2,071 in line with month. However, with the right techniques, you may boost yours significantly. Make an effort to run the numbers on your unique state of affairs, because for most retirees. Getting Social Security right is one of the most essential financial choices of their lifetime.