Credit card debt is one of the most steeply priced monetary burdens a person can bring. With interest prices frequently ranging among 20% and 30% APR, balances can spiral quickly — turning an attainable buy into a years-long legal responsibility. The best information? With the proper method and steady attempt, you could pay off credit card debt quicker than you thought. Here are the most effective approaches to help you destroy loose from high-hobby debt and reclaim your financial health.

List every debt you owe

Before you can attack your debt, you need a complete photograph of it. Write down every credit card balance, its interest fee (APR), and the minimum payment due. This simple exercise does two things: it gets rid of the anxiety of the unknown, and it enables you to prioritize which debts to address first.

Many humans are taken aback when they see the total overall laid out in front of them — and that surprise is precisely the incentive to stay committed. What subjects are readable?

Prevent adding to the balance

This sounds obvious; however, it’s the step that the general public bypasses. You cannot drain a bath with the faucet while going for walks. Whilst you are in debt-payoff mode, position your credit cards away — physically. a few human beings freeze them in a block of ice, delete saved card information from online shops, or transfer to a coins-only system for discretionary spending.

The purpose isn’t always to punish yourself. It is to create a clean boundary between your past spending conduct and the new financial conduct you’re constructing.

Use the Debt Avalanche technique

The debt avalanche method is mathematically the most green manner to cast off credit card debt. right here’s how it works:

- Pay the minimum on all of your cards each month.

- Direct any more money you may manage to pay towards the cardboard with the highest hobby price.

- As long as that card is paid off, roll that installment sum into the ensuing maximum-price card.

Due to the fact that you’re targeting the maximum high-priced debt first, you pay less in general hobby through the years. This method requires endurance — your highest-interest card can also have a massive stability — but the lengthy-time period savings can be extensive. For someone with $10,000 in debt spread throughout a couple of playing cards, the avalanche technique can keep hundreds or maybe lots of dollars in comparison to making the minimum payments.

Attempt the Debt Snowball technique rather

If motivation is your project, the debt snowball method would possibly work better for you psychologically. As opposed to concentrating on the best interest rate, you focus on the smallest balance first.

- Pay minimums on all playing cards.

- Throw extra cash on the smallest balance till it is long gone.

- Roll that freed-up expense into the ensuing littlest obligation.

Paying off a card completely — even a small one — creates an effective feel of progress. That mental win fuels the momentum to keep going. Research helps this: individuals who use the snowball approach are much more likely to stick to their debt-payoff plan because they see effects faster.

Pick out the technique that suits your personality. The quality approach is the one you will sincerely observe.

Find more money to boost Payoff

The more cash you can throw at your debt every month, the quicker it disappears. Look at your price range with sparkling eyes:

- Reduce subscriptions you no longer use or want.

- lessen dining out by meal prepping a few days every week.

- sell objects you no longer use — electronics, furniture, garments — via fb marketplace or eBay.

- take on extra profits thru freelancing, gig work, or component-time hours.

- Follow windfalls — tax refunds, bonuses, coins, presents — immediately to your debt in place of spending them.

Even a further $a hundred to $2 hundred per month makes a dramatic difference for your payoff timeline. On a $five,000 balance at 24% APR, adding simply $a hundred and fifty more per month can cut years off your repayment timetable and save hundreds in interest.

Negotiate a lower interest price

Many cardholders don’t understand that they are able to really name their credit card employer and ask for a lower APR. When you have a history of on-time payments, there is an inexpensive risk they may say yes — at least quickly.

prepare earlier than you name: recognize your current charge, point out your loyalty as a patron, and reference any competing offers you’ve seen. Even a 3% to 5% rate reduction can meaningfully lower your hobby costs and assist extra of every charge move closer to the essential.

Recall a balance switch Card

A stability switch card helps you to pass high-interest debt to a new card that gives a zero% introductory APR — frequently for 12 to 21 months. At some point of that promotional window, each greenback you pay is going without delay to reducing your debt, no longer paying interest.

This strategy works properly if:

- You have sufficient credit to qualify for a balance switch offer.

- You are disciplined enough not to rack up new charges on the antique card.

- You may realistically repay or considerably lessen the balance before the promotional period ends.

Watch for stability transfer prices, which commonly range from 3% to five% of the amount transferred. Regardless of the price, the math usually works to your advantage if you’re wearing a high-hobby stability.

Use a Debt Consolidation loan

A private loan used to consolidate credit card debt can replace numerous high-interest balances with a unmarried, lower-interest monthly payment. Personal loan prices are often significantly lower than credit card APRs, mainly for debtors with strong credit scores.

The benefits are sincere: a set monthly payment, a clear payoff date, and less money going to interest. The danger is behavioral — it’s tempting to begin the use of the now-cleared credit score cards again, turning a consolidation answer into a deeper debt hassle. If you pass this direction, decide to maintain the playing cards at a zero balance.

Automate Your Payments

Install automatic payments for as a minimum due on every card. This spares your credit score rating, dispenses with past due charges, and expels the mental burden of remembering to pay. Then, manually add any more quantities above the minimum toward your goal card every month.

Automation removes self-discipline from the equation — and self-discipline is a restrained aid.

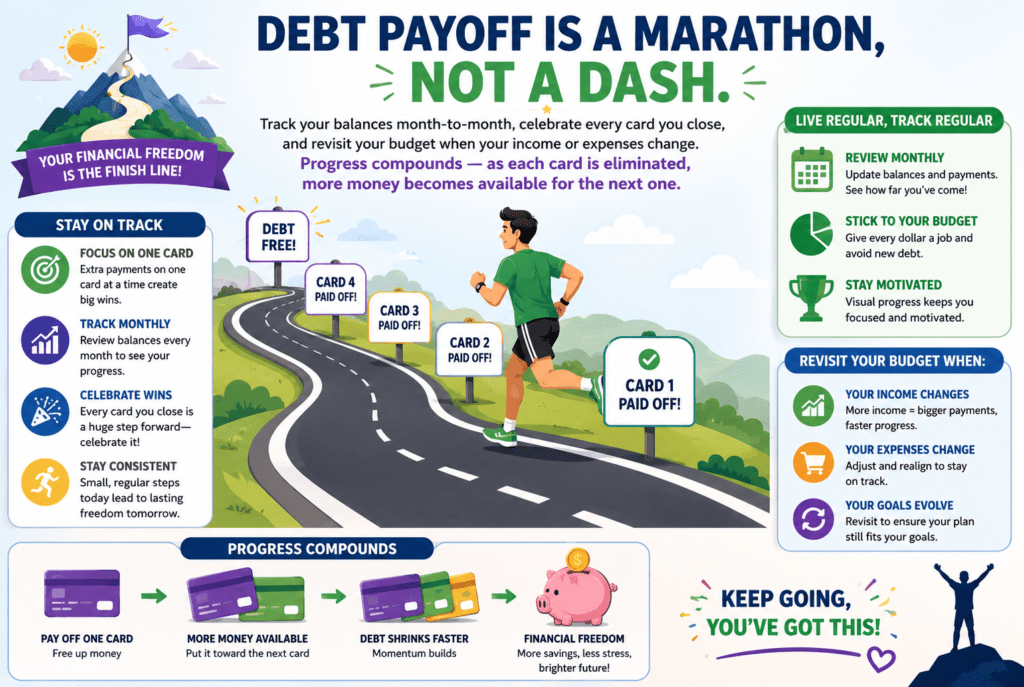

Music progress and live regularly

Debt payoff is a marathon, not a dash. Track your balances month-to-month, have fun every time you close a card, and revisit your budget as your earnings or costs change. Progress compounds — as every card is eliminated, extra money becomes available for the next one.

Conclusion

Paying off credit card debt rapidly comes down to three matters: a clean method, extra money directed at your debt, and consistency over the years. Whether or not you pick out the avalanche, the snowball, a stability transfer, or a combination of methods, the most important step is starting — nowadays, with something you have got. The sooner you begin, the less you pay in interest, and the earlier you may reach a life unfastened from high-interest debt.