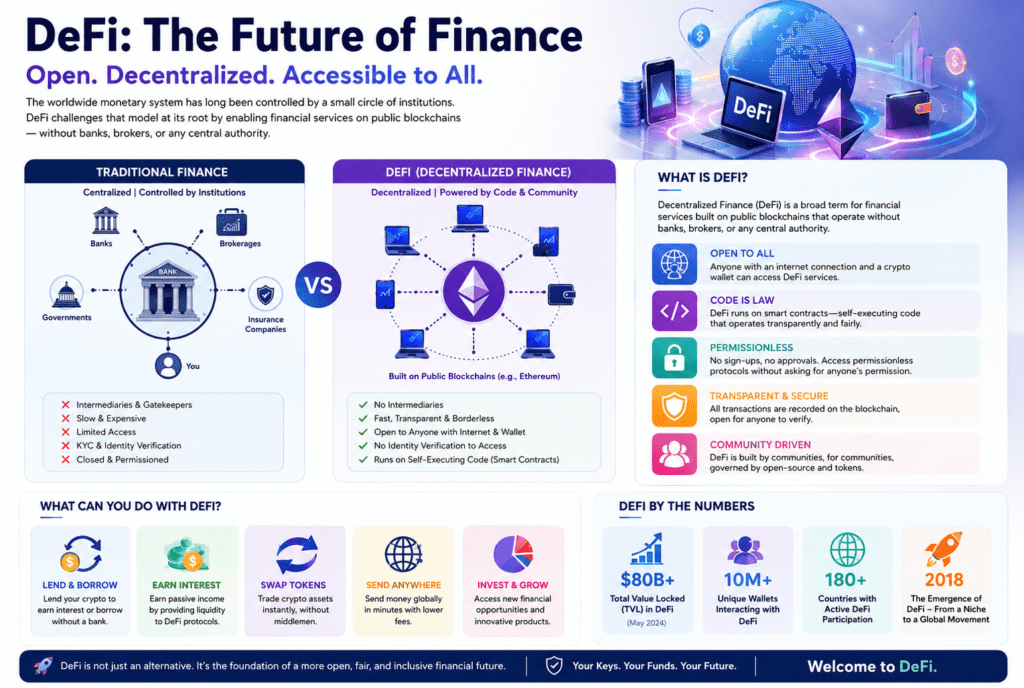

The worldwide monetary system has long been controlled by a small circle of establishments — banks, brokerages, insurance companies, and governments. For hundreds of years, in case you wanted to borrow money, earn a hobby, or send funds across borders, you had no choice but to go through them. DeFi demanding situations that model at its root.

Decentralized Finance, or DeFi, is a vast term for monetary services and products built on public blockchains — normally Ethereum — that function without banks, brokers, or any relevant authority. It’s far open to anyone with an internet connection and a crypto wallet, calls for no identity verification to access, and runs on self-executing code rather than human intermediaries. On the grounds of its emergence around 2018, DeFi has grown from a niche test into a multi-billion-dollar ecosystem reshaping how human beings consider money.

The hassle DeFi is solving

Traditional finance — regularly known as TradFi — is built on agreements in institutions. While you deposit cash in a financial institution, you accept as true with the financial institution will hold it securely, pay you interest, and return it when you ask. Whilst you send money internationally, you agree with a chain of correspondent banks to transport it efficiently. That is accepted as true with its enforcement thru law, criminal contracts, and government backstops like deposit coverage.

This system works fairly nicely in rich international locations with sturdy institutions. But for the kind of 1.4 billion unbanked adults internationally, access to is constrained by geography, documentation requirements, minimum balances, or, genuinely, a lack of local banking infrastructure. Even for people who do have access to conventional finance is gradual, high-priced, and opaque. A pass-border cord transfer can take three to five commercial enterprise days and cost a large percentage of the amount dispatched. Stock markets close on weekends. Loan approvals rely on credit score ratings that may take years to build.

DeFi proposes an exceptional architecture: replace institutional acceptance with mathematical consideration.

The Constructing Blocks of DeFi

- Blockchains

DeFi runs on blockchains — allotted ledgers maintained with the aid of heaps of computer systems worldwide. No unmarried entity controls the ledger. Transactions are recorded publicly and completely, and everybody can confirm them. Ethereum is the dominant DeFi blockchain as it helps programmable common sense; however, other chains like Solana, Avalanche, and BNB Chain have grown their own DeFi ecosystems.

- Smart Contracts

The actual engine of DeFi is the smart contract — a chunk of code deployed on a blockchain that routinely executes whilst predetermined situations are met. consider it as a merchandising device: you positioned inside the right input, the gadget delivers the output, without a cashier required.

A clever contract can be programmed to: launch a loan when collateral is deposited, distribute hobby to liquidity vendors each block, swap one token for every other at a calculated charge, or liquidate a position while it falls below a sure price. As soon as deployed, the contract runs exactly as written. No person can regulate it, freeze it, or selectively follow it. This immutability is both DeFi’s finest energy and one among its key dangers — if the code has a Trojan horse, it cannot effortlessly be patched.

- Wallets and Keys

Customers interact with DeFi through crypto wallets like MetaMask or agree with wallet. These wallets hold non-public keys — cryptographic passwords that show ownership of assets. There may be no username or password restoration. Whoever holds the non-public key controls the finances. That is the self-custody version: you are your own financial institution.

Center DeFi applications

- Decentralized Exchanges (DEXs)

Traditional exchanges like the Big Apple inventory change suit shoppers and sellers thru an order book controlled by a relevant corporation. DEXs like Uniswap and Curve replace the order book with an algorithm called an automated market Maker (AMM). Liquidity carriers deposit pairs of tokens right into a pool. The AMM formulation — normally x × y = ok — automatically prices trades based on the ratio of tokens inside the pool. Trades execute immediately, across the clock, without a signal-up required.

- Lending and Borrowing

Protocols like Aave and Compound allow customers to lend their crypto belongings and earn interest, or borrow against collateral. The whole thing is over collateralized — in case you need to borrow $500 well worth of stablecoins, you may want to deposit $750 well worth of Ethereum as collateral. If the collateral falls below a sure threshold, the protocol robotically liquidates it to repay the mortgage. No credit check, no office work, no ready period.

- Stablecoins

Volatility is DeFi’s practical enemy. Bitcoin rising or falling 10% in an afternoon makes it a bad medium for lending, buying, and selling. Stablecoins resolve this by pegging their price to a strong asset, usually the United States dollar. Some stablecoins, like USDC, are subsidized 1:1 by using actual greenbacks held in a bank. Others, like DAI, are generated by over-collateralizing crypto belongings in a smart agreement — entirely on-chain with no bank involved. Stablecoins are the lifeblood of DeFi, allowing dollar-denominated pastime in a trustless environment.

Yield Farming and Liquidity Mining

Yield farming entails deploying crypto belongings throughout a couple of DeFi protocols to maximize returns. Users would possibly deposit tokens right into a liquidity pool, acquire LP (liquidity provider) tokens in return, and then stake those LP tokens in a separate protocol to earn additional rewards. Liquidity mining in particular refers to earning a protocol’s native governance token as a reward for presenting liquidity. These techniques can generate excessive yields — but deliver compounding dangers.

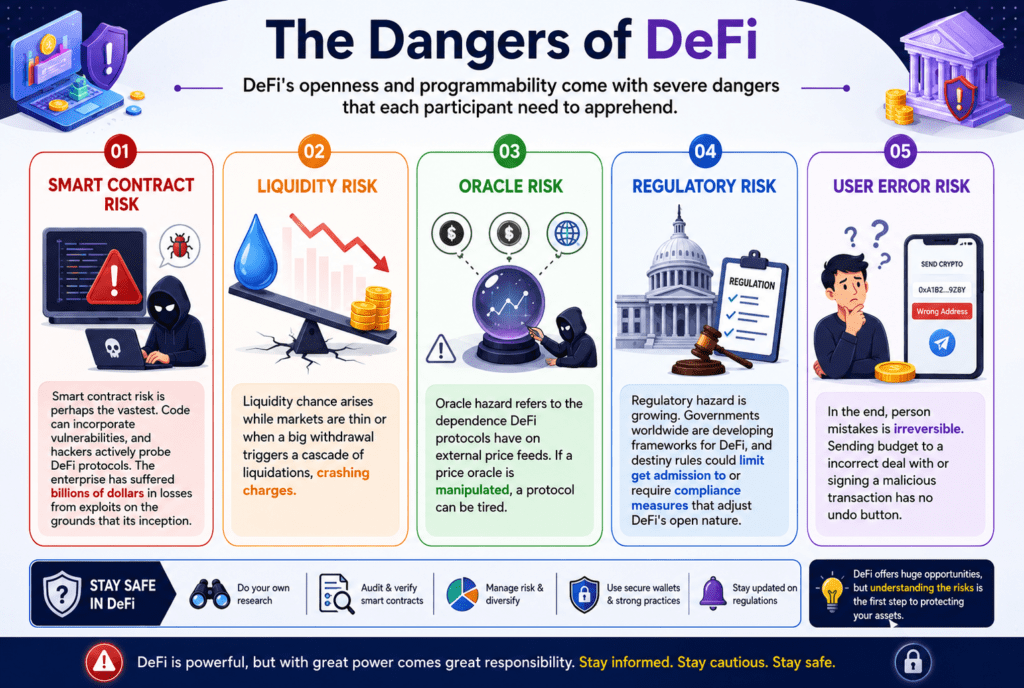

The dangers of DeFi

DeFi’s openness and programmability come with severe dangers that each participant needs to apprehend.

- Clever settlement threat is perhaps the vastest. Code can incorporate vulnerabilities, and hackers actively probe DeFi protocols. The enterprise has suffered billions of dollars in losses from exploits on the grounds that its inception.

- Liquidity chance arises while markets are thin or when a big withdrawal triggers a cascade of liquidations, crashing charges.

- Oracle hazard refers to the dependence that DeFi protocols have on external price feeds. If a price oracle is manipulated, a protocol can be compromised.

- Regulatory hazard is growing. Governments worldwide are developing frameworks for DeFi, and destiny rules could limit access or require compliance measures that adjust DeFi’s open nature.

In the end, a person’s mistakes are irreversible. Sending budget to an incorrect deal with or signing a malicious transaction has no undo button.

Conclusion

No matter its dangers, DeFi represents a real shift in economic structure. It demonstrates that complicated economic services — lending, trading, derivatives, insurance — can be delivered via open, auditable code as opposed to opaque establishments. For customers in countries with unstable currencies or restricted banking access, DeFi gives a dollar-denominated financial device on hand from a telephone.

DeFi is not yet an alternative to traditional finance. It is risky, technically complicated, and carries actual risks. However, as the infrastructure matures and consumer experience improves, its middle proposition — economic services which are open, transparent, and governed by way of code in preference to gatekeepers — will only end up more compelling.

The question is no longer whether decentralized finance is possible. It truly is. The query is how far it’ll pass.