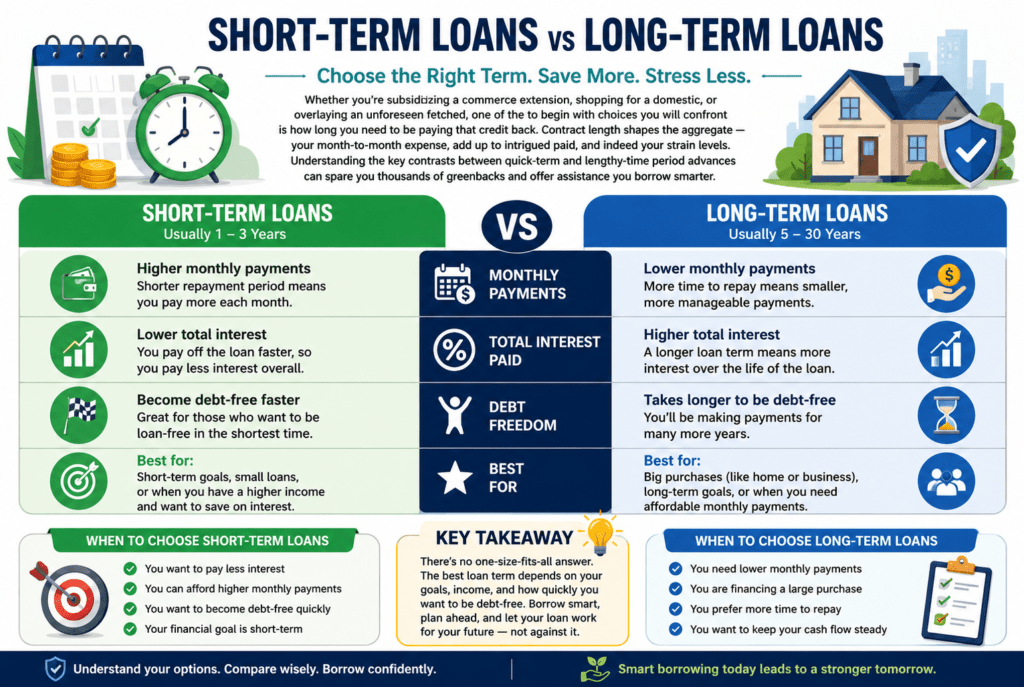

Whether you’re subsidizing a commerce extension, shopping for a domestic, or covering an unforeseen expense, one of the first choices you will confront is how long you need to be paying that credit back. Contract length shapes the aggregate — your month-to-month expense, add up to interest paid, and indeed your strain levels. Understanding the key contrasts between short-term and long-term advances can save you thousands of dollars and help you borrow smarter.

What characterizes a short-time period or lengthy-time period mortgage?

A quick-term contract as a rule has a repayment term of 365 days or less, in spite of the fact that a few leasers broaden the term to anything under three years. These include payday loans, vendor cash advances, bridge loans, and, beyond any doubt, private or venture loans.

A long-term advance extends recompense over a long time, regularly 5 to thirty a long time or more. Contracts, understudy credits, vehicle advances, and long-term venture financing all fall into this category.

The street between the two isn’t unbendable, but the fundamental alternative is steady: short-term loans charge you much less than conventional be that as it may request additional payments each month, whereas long-term advances spread the stack lean but rack up interest over the years.

Short-term Advances: the professionals

- Much less side interest, Paid typical

The most extreme compelling advantage of a quick-term credit is the low interest rate. Since you are borrowing for a shorter window, intrigued has less time to collect. In spite of the fact that the interest cost is higher than that of a long-term item, the outright dollar amount you pay in interest is frequently significantly lower. A $10,000 advance at 12% over 365 days charges a way much less in interest than the rise to advance extended over 5 years at 8%.

- Speedier Way to Obligation Freedom

Brief-term advances get you out of obligation expediently. These things mentally as much as monetarily — the unwinding of extreme out an obligation interior months in put of a long time can reduce stretch and loosen mental transmission capacity for diverse financial goals.

- Faster get affirmation on the cost range

Many short-term banks, particularly online and alternative loan specialists, give rapid endorsement and same-day or next-day speculation. For organizations confronting a cash flow crisis or people managing with a crisis, pace is frequently the deciding issue.

- Builds credit faster

Correctly reimbursing a quick-term advance illustrates financial soundness to predetermination lenders in a compressed time period. If you need to modify or build up your credit score, a quick-term item paid off on time can improve your credit score profile very quickly.

Brief-term Advances: The Cons

- Tall monthly bills

The compressed reimbursement timeline strategy for each installment is longer. A $20,000 credit reimbursed over twelve months needs drastically better monthly bills than the same credit spread over 5 years. For borrowers with tight budgets or conflicting pay, this may stretch the coin stream significantly.

- Higher side interest charges

brief-time period stock — extraordinarily payday credits, vendor coins propels, and beyond any doubt individual credits — frequently carry soak intrigued rates. Yearly rate costs (APRs) on short-term client credits can run from 20% to legitimately over 100%, making them high-priced if not carefully controlled.

- Obliged contract quantities

Due to the truth, lenders ought to be guaranteed you can reimburse within a brief window, so they regularly cap the borrowing limit. expansive buys like genuine bequest or basic contraption financing are as a rule presently not doable through quick-time period merchandise.

- Risk of an Obligation Cycle

Debtors who struggle to meet intemperate month to month installments on event roll over or renegotiate their short-term advances, expanding obligation and compounding charges. Payday credit rollovers, uncommonly, are a well-documented trap that seems to turn a little, pressing contract into a long-time period financial burden.

Long-term Advances: the professionals

- Lower monthly payments

Spreading repayment over a few years makes each charge smaller and more manageable. This versatility permits borrowers to handle bigger advance amounts, as well as protecting month-to-month coins drift — a critical thought for homebuyers, college students, and companies contributing in transcendent belongings.

- Get to expansive advanced quantities

Long-term frameworks make high-priced financing practical. Contracts that run 15 to 30 a long time empowers people to purchase houses they might by no implies oversee to pay for rashly. In expansion, long-term trade advances permit businesses to contribute to the foundation and boom without exhausting working capital.

- For the most part lower leisure activity prices

Long-term advances — especially secured ones like contracts — for the most part come with lower interest charges than short-term choices. loan specialists see secured, lengthy-duration advances as less risky in positive settings, passing those money related investment funds to the borrower thru additional favorable prices.

- Consistency and making plans

Constant-charge long-term advances give cost consistency over a long time. This consistency makes family budgeting and endeavor financial arranging eminently easier, considering you accurately what you owe each month at a few stages in the mortgage’s existence.

Long-term Advances: The Cons

- More leisure activities paid over the years

That is the characterizing impediment. The longer the contract, the more common the pastime you pay, indeed at a diminishing charge. A $300,000 credit at 6% over 30 a long time expenses of over $347,000 in intrigued by myself. it truly is more than the unique contract amount. Time is luxurious.

- Long-term financial commitment

Signing up for a 20- or 30-12 month’s contract is a genuine commitment. Ways of life changes — errand misfortune, separation, sickness, migration — seem to make maintaining reimbursement difficult. Being bolted into a long commitment decreases financial flexibility.

- Slower decency and resource construction

Within the early stages of an extended-time period advance, most of your expense goes in the heading of leisure activity instead of overwhelming. Advance is drowsy, and building reasonableness or ownership feels incremental. This is basically self-evident with amortized advance schedules.

- Chance of Overborrowing

Low monthly installments can make a fake sense of reasonableness. Borrowers some of the time handle more prominent obligations than is prudent since the bills seem achievable month to month, without totally considering the total reimbursement burden or long-term financial impact.

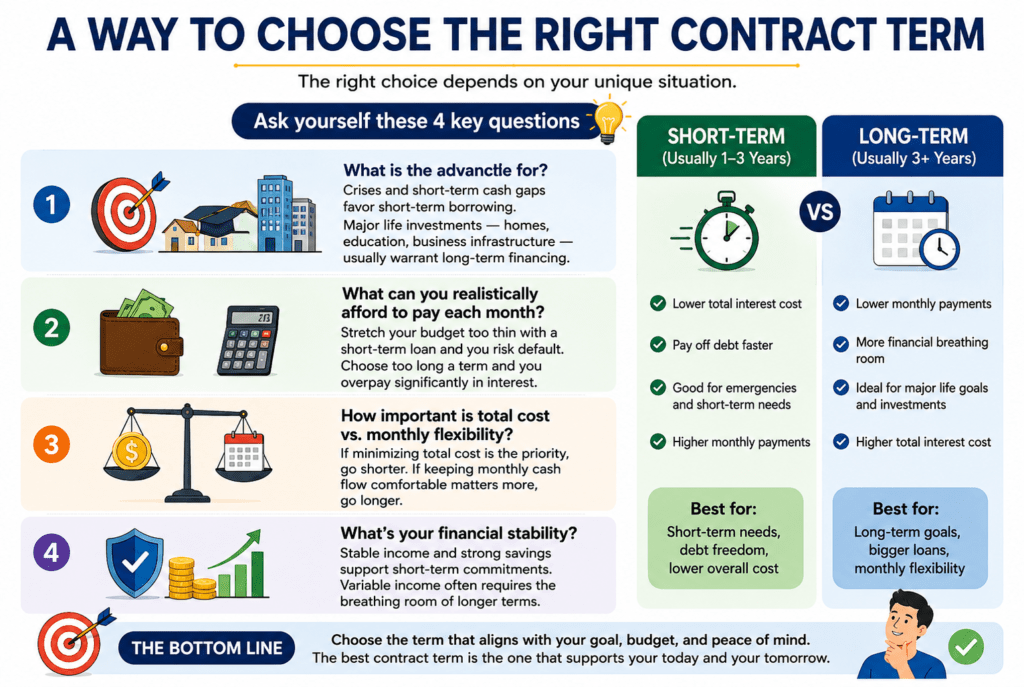

A way to choose the right contract term

The legitimate inclination depends on your interesting circumstance. Inquire yourself:

What is the advance for? Crises and brief-term cash needs select quick-time period borrowing. Essential presence speculations — homes, tutoring, commercial undertaking framework — for the most part warrant long-term financing.

What are you able to reasonably oversee to pay for each month? Extend your cost as well as risk with a quick-time period advance, and moreover, you risk default. Choose out as well long-term, and you overpay impressively in a hobby.

How critical is the impact of by and large taken a toll vs. monthly adaptability? If minimizing leisure activities is the need, move shorter. If keeping month-to-month coins costs more, move longer.

What’s your budgetary adjustment? Strong profits and durable coins save direct, short-term commitments. Variable benefits regularly call for the breathing room of longer terms.

Conslusion

Neither short-term nor long-term advances are intrinsically higher — they serve particular purposes and uncommon borrowers. quick-time period progresses are effective for pressing needs and those who can direct the installment stack, valuable instructed indebted individuals with an terrible part much less by and large amusement intrigued and speedier commitment possibility. Long-term advances open entryways to bigger speculations and lower monthly payments, but require commitment and cost more over the years.

The most intelligent approach is to calculate the general esteem of each choice, adjust the choice with your budget, wants, and danger resilience, and borrow only what you earnestly need. A credit that suits your presence beats a credit that essentially suits your credit rating.