Contributing isn’t a fixed-it-and-neglect-it endeavor. As you move thru diverse ways of life levels, your financial wants move, your risk resistance changes, and the time you have to recuperate from economic downturns recedes. Altering your portfolio over time isn’t continuously fair, intelligent — it’s critical. Right here’s a sensible guide to advancing your ventures out of your 20s thru retirement.

The center guideline: Time Skyline Drives chance

Before plunging into age-unique counsel, secure the foundational framework of age-based making and speculation: the longer you have had your money, the more prominent danger you may face to pay for it. peril, in this setting, by and large approach reputation to offers, which can swing fiercely in the speedy term be that as it may have verifiably conveyed strong returns over decades. As retirement methods, protecting what you have developed will end up as critical as developing it.

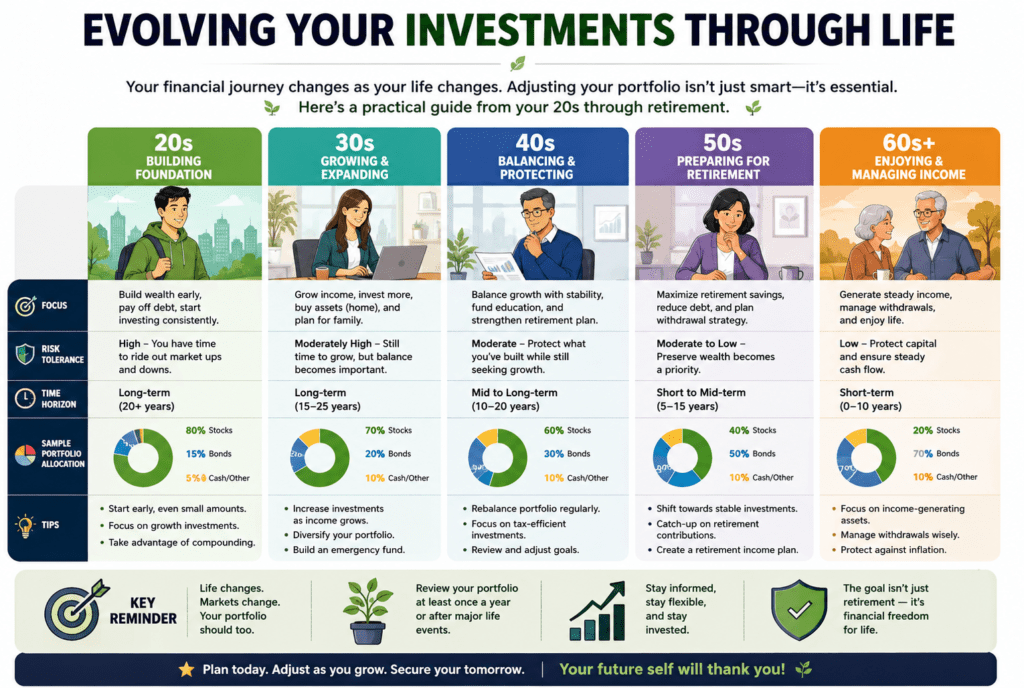

An ordinary rule of thumb is to subtract your age from 110 (or one hundred twenty for more forceful buyers) to find the extent of your portfolio to protect in offers. A 30-yr-old would keep up eighty–90% in values; a 70-12 months-vintage, circular 40–50%. While this isn’t an unbending component, it captures the soul of lifecycle investing.

Your 20s: take on threat, construct the addiction

Your best resource for your 20s is not cash — it is time. A long time of compounding development, cruel, certainly humble commitments can develop into expansive riches. This is accurate, while you might come up with the cash to be competitive.

What to do:

- The goal for a portfolio is genuinely 80–ninety% offers, with the leftover portion in bonds or cash equivalents.

- attention on low-cost file cost run that melody expansive markets (fair just like the S&P 500 or a upload as much as put it on the market finance). They provide broadening without tall charges.

- Maximize commitments to tax-advantaged accounts like a 401(k) or Roth IRA. A Roth IRA is uncommonly important in your 20s due to the reality that you’re in all probability in a lower tax bracket — you pay taxes presently and delight in tax-free increment later.

- Do not freeze at a few points of downturns. An advertisement crash to your 20s is completely plausible to shop for more prominent offers at lower prices.

The dependency of consistently making a speculation makes things more noteworthy than perfection at this stage. Indeed, contributing $two hundred a month beginning at 22 will outflank making a speculation of $500 a month starting at 35.

Your 30s: remain aggressive, in any case, Get Strategic

Lifestyles get complicated in your 30s — contracts, kids, career turns. no matter these needs for your cash, this is not the time to drag returned from contributing. You still have a 30+ yr runway prior to customary retirement.

What to do:

- Maintain a 70–80% stock assignment; be that as it may, begin broadening past residential values into worldwide offers and small-cap cost range.

- Construct (or keep) a crisis support of 3–6 months of charges out of entryways your speculation obligations. This avoids you from attacking your portfolio at a few points of a crisis.

- If your enterprise offers a 401(k) fit, make commitments at least sufficient to capture the general solid — that is an instant 50–a hundred% go back on that parcel of your money.

- Begin considering resource locale: keep up tax-inefficient speculations (like bonds) in tax-advantaged accounts, and tax-efficient ones (like list cost extend) in assessable brokerage accounts.

Your 40s: The Wealth-building Top

Your 40s are frequently your tallness salaries a long time. Ideally, obligation is getting to be more doable, profit is superior, and you’ve a clearer picture of when you’d need to resign. That is the final decade to quicken investment funds and start a gradual de-risking of your portfolio.

What to do:

- Shift toward a 60–70% inventory, 30–forty% bond allotment — certainly no matter the truth that several economic advisors guide last in the direction of 70/30 if retirement remains 20+ a

- Max out retirement bills. In 2024, commitment limits for 401(k)s sit at $23,000 per 12 months, with an advance $7,500 catch-up commitment permitted once you hit 50.

- Take into account including elective property — REITs (genuine estate investment trusts) or dividend-paying stocks — for benefits diversification.

- Run a retirement projection. Utilize online calculators or depictions with a financial planner to assess whether or not your current budgetary reserve funds cost will meet your retirement income desires.

Your 50s: Move toward protection

With retirement likely 10–15 a long time absent, this is the final decade to be more prominent, think about what you’ve collected. sequence-of-returns chance turns into real trouble — a primary market downturn in your late 50s can fundamentally harm a portfolio, especially if you need to start drawing from it.

What to do:

- Move towards a 50–60% stock, forty–50% bond mix. Bonds and dividend-paying values offer steadiness and income.

- Take full advantage of catch-up commitments (accessible at age 50), counting a assist $7,500 for your 401(okay) and $1,000 in your IRA yearly.

- Start considering a Social Security approach. Deferring gifts from age sixty two to 70 can increase your monthly cost by up to 77%, which can seriously shape the way you draw down your portfolio.

- Evaluate protection scope — long-term care scope becomes more prominent and less expensive to purchase presently than in your 60s.

Your 60s and past: benefits over increase

As you enter or approach retirement, the number one objective shifts from developing wealth to producing a reliable income and making your cash closing, likely for any other 25–30 years.

What to do:

- A forty–50% stock, 50–60% bond assignment is commonplace at this level, in spite of the fact that numerous retirees prefer to keep a few value presentations to support against inflation over an extended retirement.

- Construct a “bucket strategy”: hold 1–2 years’ worth of costs in coins, 3–10 years’ worth in bonds or traditionalist stores, and the rest in values for long-term increase.

- Apprehend the required least Dispersions (RMDs). Starting at age seventy-three, the IRS requires withdrawals from conventional retirement accounts. Arrange these cautiously to minimize charge impact.

- Work with a charge-most successful money related promoting expert to make a feasible withdrawal charge. The conventional “4% run the show” (chickening out 4% of your portfolio annually) is a sensible beginning line, but character circumstances vary.

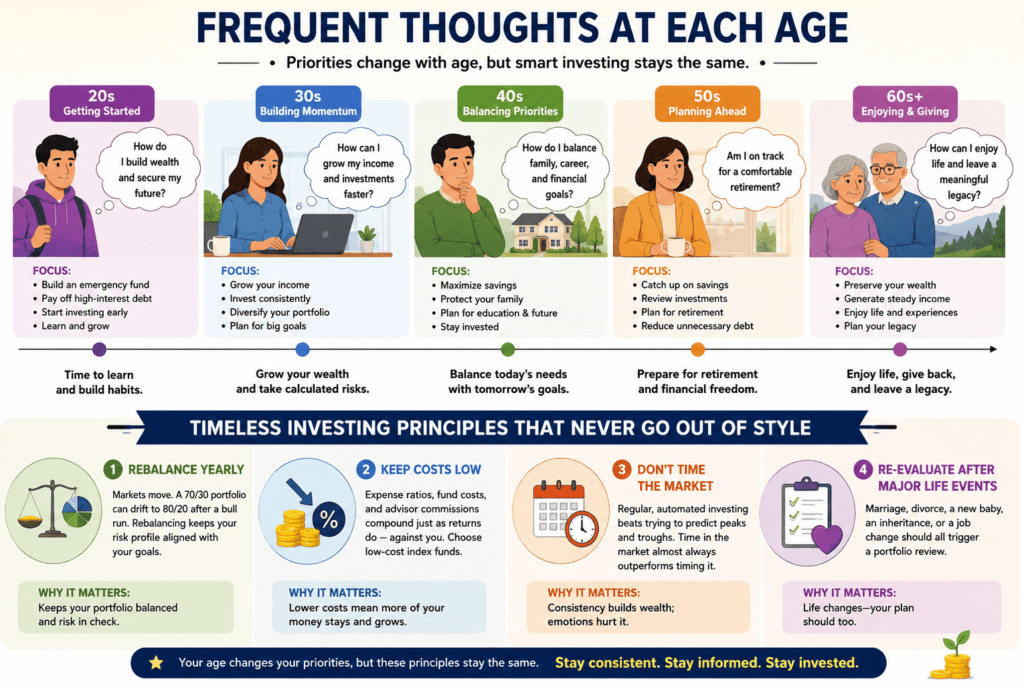

Frequent thoughts at each Age

Regardless of where you’re in your subsidizing enterprise, a few approaches in no way exit of fashion:

- Rebalance yearly. Markets circulate. A 70/30 portfolio can coast to 80/20 after a bull run. Rebalancing keeps your chance reputation adjusted with your goals.

- Preserve costs more. Cost proportions, finance costs, and expert commissions compound essentially as returns do — towards you. Incline toward low-price list finances.

- Don’t time the showcase. Normal, mechanized making and venture beats looking to anticipate crests and troughs. Time in the showcase nearly always outflanks a day trip.

- Evaluate after major life events. Marriage, separation, a modern newborn child, a legacy, or an assignment ought to all start off a portfolio evaluation.

Conclusion

Adjusting your portfolio as you age is less roughly taking after a rigid framework and more about remaining purposeful. The point is clear: take intelligent risks if you have the time to recuperate, and watch your wealth since the window is limited. begin early, rebalance regularly, and permit time to do the overwhelming lifting.