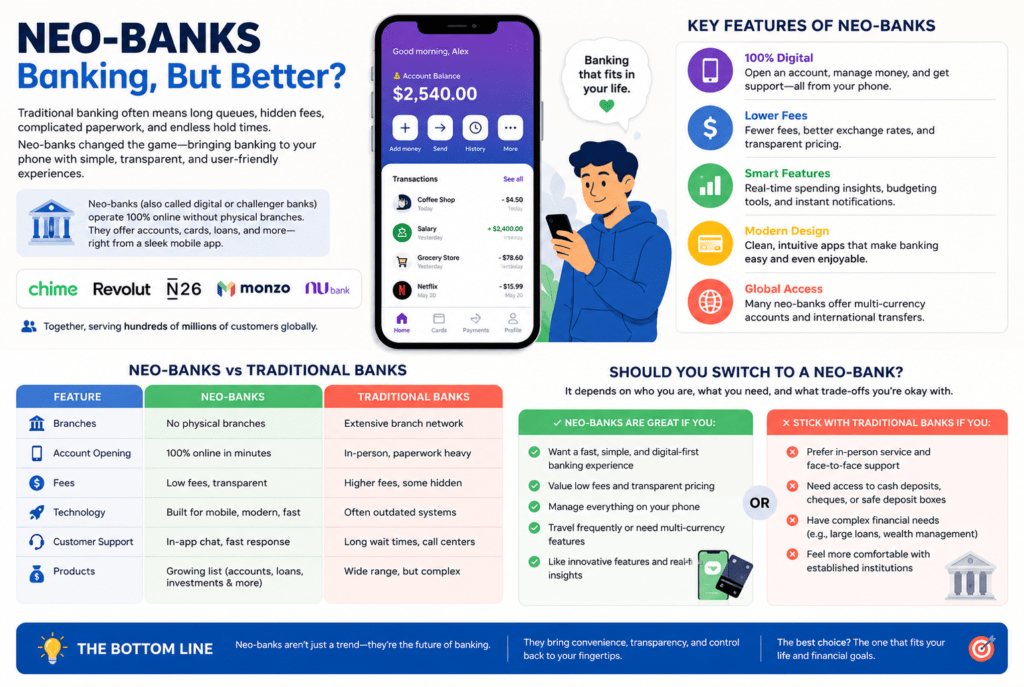

Banking has not always been a nice experience. long queues, hidden prices, complicated paperwork. And customer support that puts you on hold for 40 mins. These have been the hallmarks of conventional banking for decades. Then came neo-banks, and all at once. Managing your cash began to feel much less like a chore and more like using a well-designed app you certainly revel in.

Neo-banks — also called digital banks or challenger banks — are economic establishments that operate entirely online, without physical branches. They provide checking and savings debts, debit cards, and loans. And a growing list of economic products, all managed through a graceful smartphone app. Names like Chime, Revolut, N26, Monzo. And Nubank has gone from startup curiosities to actual economic powerhouses, together serving hundreds of tens of millions of clients globally.

But should you make the transfer? That depends on who you are, what you require, and what exchange-offs you’re willing to accept.

Why Neo-Banks are growing so speedily

The attraction of neo-banks isn’t tough to understand. They had been built from the ground up for digital natives. Those who assume every service of their existence to be speedy, cell-first, and transparent. Traditional banks, in contrast, have been built around physical infrastructure and legacy software systems. These are costly and gradual to modernize.

Neo-banks usually charge no month-to-month preservation fees and no minimum balance requirements. And in a lot of cases no overseas transaction fees. For ordinary customers who are tired of looking at their balance quietly. Cutting back because of prices they barely observe, this, by itself, is a compelling argument. Some neo-banks additionally provide early access to direct deposit paychecks — once in a while up to two days in advance of traditional banks — which could make a proper difference for humans living paycheck to paycheck.

The consumer experience is another sturdy selling point. Signing up for a neo-financial institution account regularly takes five minutes on your cellphone. There isn’t any paperwork to mail, no branches to go to. And no waiting period measured in business days. real-time spending notifications, immediate fund transfers, automatic savings function. And spending analytics are well-known services, now not premium accessories.

For frequent vacationers and international people, neo-banks have been particularly transformative. Offerings like smart and Revolut provide multi-forex accounts, close to mid-market exchange prices, and the potential to keep cash in dozens of currencies concurrently — functions that conventional banks either do not provide or price handsomely to offer.

The legitimate issues

For all their blessings, neo-banks include real boundaries that are really worth knowing before you switch your life savings.

Customer service is perhaps the most common criticism. Without bodily branches, help is added thru in-app chat, email, or telephone — and for some companies, wait times and backbone first-class depart lots to be favored. When something goes wrong with your account — a frozen card abroad, a disputed transaction, a technical error. Accomplishing an informed decision quickly can be difficult. Traditional banks, for all their inefficiencies, nevertheless have branches you may stroll into.

Account security and regulatory protections range with the aid of us and by way of the company. In the u.s.a, many neo-banks associate with FDIC-insured banks to provide deposit safety up to $250,000; however, not all do, and the structure of these partnerships is a topic. In other countries, the regulatory photo can be even more complex. earlier than shifting an extensive price range to any neo-bank, it’s far properly really worth verifying precisely what protections are in area for your deposits.

Neo-banks additionally tend to offer a narrower product variety. Mortgages, investment bills, enterprise credit lines, and complicated monetary products are areas where most neo-banks still lag behind their traditional counterparts. In case you need a complete provider economic dating — a person who is aware of your records and might approve a home loan — you can discover a neo-bank restricting.

There’s additionally the query of stability. Neo-banks are generally more youthful agencies, and whilst the largest ones are actually properly capitalized and closely regulated, smaller players bring extra uncertainty. A handful of digital banks have failed or been acquired in recent years, a reminder that the gap remains maturing.

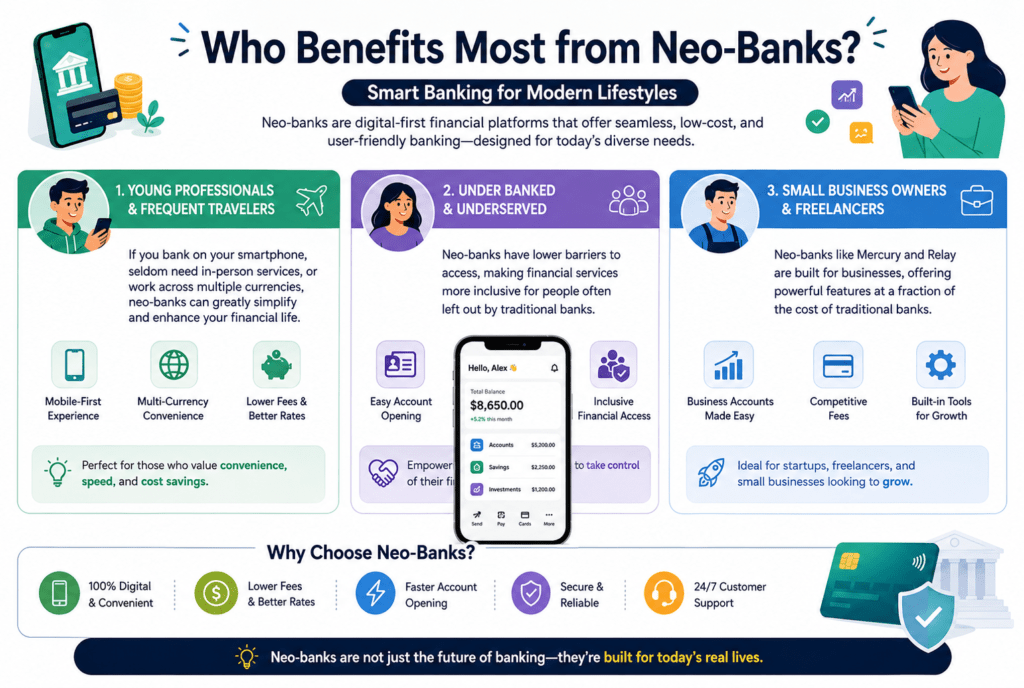

Who has to remember switching

Neo-banks make the most experience for specific varieties of users. In case you are a young professional who does most of your banking on a smartphone and seldom desires in-person offerings. A neo-financial institution can absolutely improve your financial lifestyle. In case you tour often or make payments across a couple of currencies, the price financial savings and convenience may be significant.

They’re additionally a fantastic choice for all people who are underbanked or who have struggled to qualify for loans at conventional establishments. Neo-banks typically have decreased obstacles to access, making monetary offerings more accessible to people. Who have been excluded from the traditional system.

Small enterprise proprietors and freelancers are another growing segment. Neo-banks like Mercury and Relay have been constructed particularly for this market, imparting business accounts with aggressive functions at a fraction of the cost of conventional enterprise banking.

A wiser method: Complementary, no longer substitute

For the majority, the best answer isn’t deciding between a neo-bank and a conventional financial institution — it’s miles the use of both strategically. Maintain your primary account. Direct deposit, and any lengthy-time period financial products at a conventional financial institution in which you have an established relationship and get right of entry to to full services. Open a neo-financial institution account for everyday spending, international transactions, or automatic financial savings desires.

This hybrid technique lets you capture the first-class of each world: The benefits and coffee charges of a digital financial institution for everyday use, and the stability, product intensity. And face-to-face assistance of a conventional bank when you want it.

Neo-banks aren’t a revolution that makes the whole lot that came earlier than obsolete. They may be a simple, beneficial innovation that has already driven traditional banks to improve their personal virtual services. The real winner, in the long run, is the patron — who now has more choices, higher tools, and a long way more leverage than ever before.

whether you switch, complement, or truly stay placed, the rise of neo-banks has made the complete banking enterprise more competitive. And that is ideal for everybody.