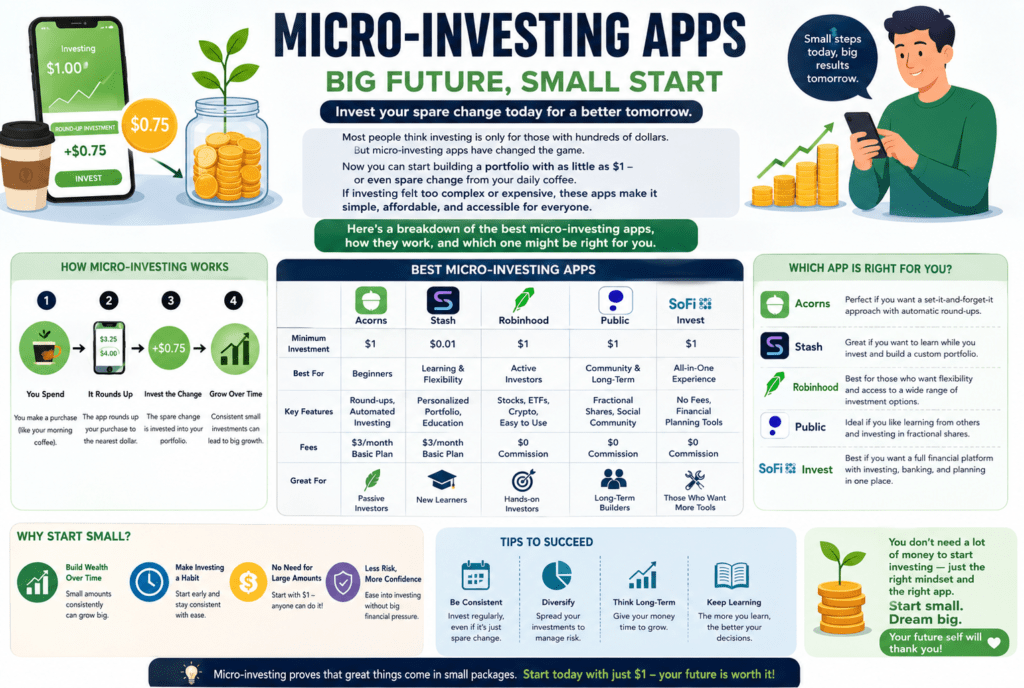

most of the people count on making an investment, which is most effective for those with hundreds of dollars sitting in a financial savings account. However, micro-making an investment app has absolutely flipped that idea. Nowadays, you could begin building a portfolio with as little as a dollar — or maybe just the spare trade out of your morning coffee. If you’ve been avoiding investing because it felt too complex or too highly-priced, Spare Exchange apps might be exactly what you need to get started.

Here’s a breakdown of the quality micro-making an investment apps available right now, how they work, and which one might be the right in shape for your financial goals.

What’s Micro-making an investment?

Micro-investing is the exercise of investing very small quantities of money — occasionally simply cents — on a regular basis. Spare change apps take this a step further by automatically rounding up your ordinary purchases to the closest dollar and making an investment of the difference. Spend $three.60 on a snack? The app rounds it up to $four.00 and invests that $0.40 for you.

Through the years, these tiny quantities add up. Combined with a compound hobby and steady contributions, micro-investing may be a quite powerful way to build wealth without feeling the pinch in your day-to-day budget.

Acorns — great average for novices

Acorns is arguably the most famous spare change app available on the market, and for top cause. It pioneered the round-up model and has, for this reason, grown into a full economic environment.

How it works: You link your debit or credit cards, and Acorns routinely rounds up every buy. Once your spare exchange accumulates to $5, it’s invested right into a diversified portfolio of ETFs based on your risk tolerance — from conservative to aggressive.

What makes it stand out: Acorns additionally gives a “observed cash” characteristic in which associate brands make investments to your behalf when you shop with them. The app has three plan ranges — private, non-public Plus, and top class — starting at $three per month. For small account balances, the month-to-month rate can devour into returns, so it really works satisfactorily for folks who also make recurring contributions.

nice for: Absolute novices who want a totally automatic, hands-off investing experience.

Stash — satisfactory for studying while investing

Stash combines micro-investing with economic schooling, making it a strong choose for folks that want to recognize what they’re making an investment in instead of simply handing money over to a set of rules.

Unlike Acorns, Stash lets you pick out your very own investments from a curated library of shares and ETFs, many of which might be supplied with plain-language descriptions and themed portfolios (like “smooth & green” or “American Innovators”). This offers beginners an extra energetic role in their financial journey.

What makes it stand out: Stash additionally gives a stock-lower back debit card that rewards you with fractional shares of the brands you save at. Plans begin at $three per month, and the app includes a retirement account choice and a custodial account for children.

Best for: Curious beginners who want training along with their investments.

Robinhood — exceptional for commission-free inventory buying and selling

Robinhood changed the investing world by way of eliminating buying and selling commissions, and it stays one of the most popular platforms for hands-on micro-investors. Even as it is now not a traditional spare change app, its fractional shares function — called “Slices” — lets you purchase partial shares of principal businesses for as little as $1.

What makes it stand out: Robinhood has no month-to-month subscription fee for its fundamental plan, which is a substantial benefit for people with smaller balances. It offers stocks, ETFs, options, and cryptocurrency — all in one easy, smooth-to-use interface. Its Robinhood Gold plan ($five/month) unlocks margin making an investment and top rate marketplace records.

great for: newbie to intermediate traders who want greater control over where their money is going without paying commissions.

Public — fine for Social making an investment

The public takes a unique approach by means of blending making an investment with a social community. You can follow different buyers, see what they’re shopping for, and discuss market actions — all within the app.

Like Robinhood, Public offers fractional stocks starting at $1, fee-free buying and selling on stocks and ETFs, and no account minimum. It additionally helps alternative assets like treasuries and high-yield cash debts.

What makes it stand out: Public is completely fee-free and doesn’t promote order, go with the flow to market makers, which the employer argues gives users fairer prices. The social feed is, in reality, a beneficial device for more recent buyers who learn better via community dialogue.

pleasant for: younger traders who like getting to know from a network and want transparency in how trades are accomplished.

SoFi makes investments — quality for an All-in-One financial App

SoFi began as a student loan refinancing company but has expanded into a complete financial platform. Invest lets customers buy fractional stocks, automate routine investments, and get access to active and automatic (robo-guide) investing — all without using control charges.

What makes it stand out: SoFi contributors get access to a number of perks, which include career coaching, financial planning classes, and fee discounts on different SoFi merchandise. The app also gives crypto, IPO access, and an excessive-yield financial savings account, making it an effective hub in case you need to manage all of your budget in one place.

exceptional for: people who want a complete economic atmosphere beyond just investing.

Betterment — quality Robo-guide for Micro-investors

Betterment is one of the original robo-advisors, and it remains one of the first-rate for fingers-off traders who want smart, automated portfolio management. There may be no minimum to open an account, and the app routinely rebalances your portfolio and harvests tax losses to enhance your after-tax returns.

What makes it stand out: Betterment prices zero.25% yearly in your balance (now not a flat monthly rate), which makes it surprisingly cost-effective for those with developing account balances. It additionally offers socially responsible investment portfolios and a top-rate plan with limitless access to financial advisors.

satisfactory for: investors who need an advanced robo-marketing consultant without the excessive minimums of conventional wealth managers.

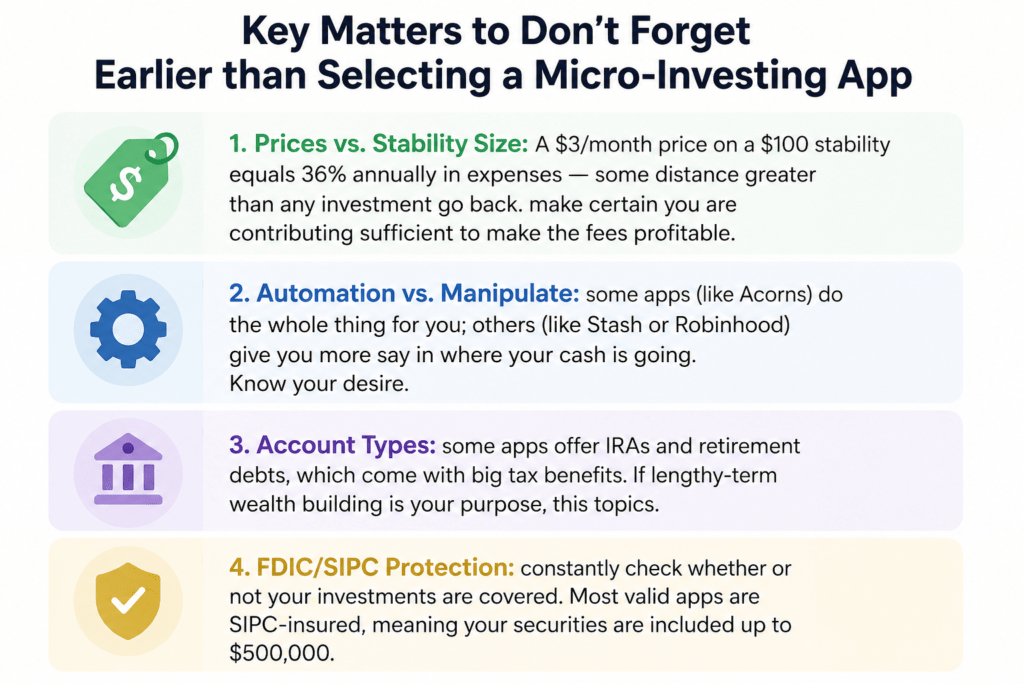

Key matters to don’t forget earlier than selecting a Micro-investing App:

prices vs. stability size: A $3/month price on a $a hundred stability equals 36% annually in expenses, much greater than any investment return. Make certain you are contributing sufficient to make the fees profitable.

Automation vs. manipulation: some apps (like Acorns) do the whole thing for you; others (like Stash or Robinhood) give you more say in where your cash is going. Know your desire.

Account types: some apps offer IRAs and retirement debts, which come with big tax benefits. If lengthy-term wealth building is your purpose, this topics.

FDIC/SIPC protection: constantly check whether or not your investments are covered. Most valid apps are SIPC-insured, meaning your securities are included up to $500,000.

Conclusion

Micro-investing apps have removed every excuse not to begin. No big savings required, no monetary information wanted, no complicated setup — just your smartphone and the spare exchange you are already spending.

The secret’s consistency. Some cents here and a greenback there can also seem insignificant, but over months and years, compounding turns small contributions into real wealth. The habit you construct nowadays is worth a long way greater than the quantity you invest.

Choose one app from this list, link your card, and start. Your future self will thanks for no longer waiting to any extent further.