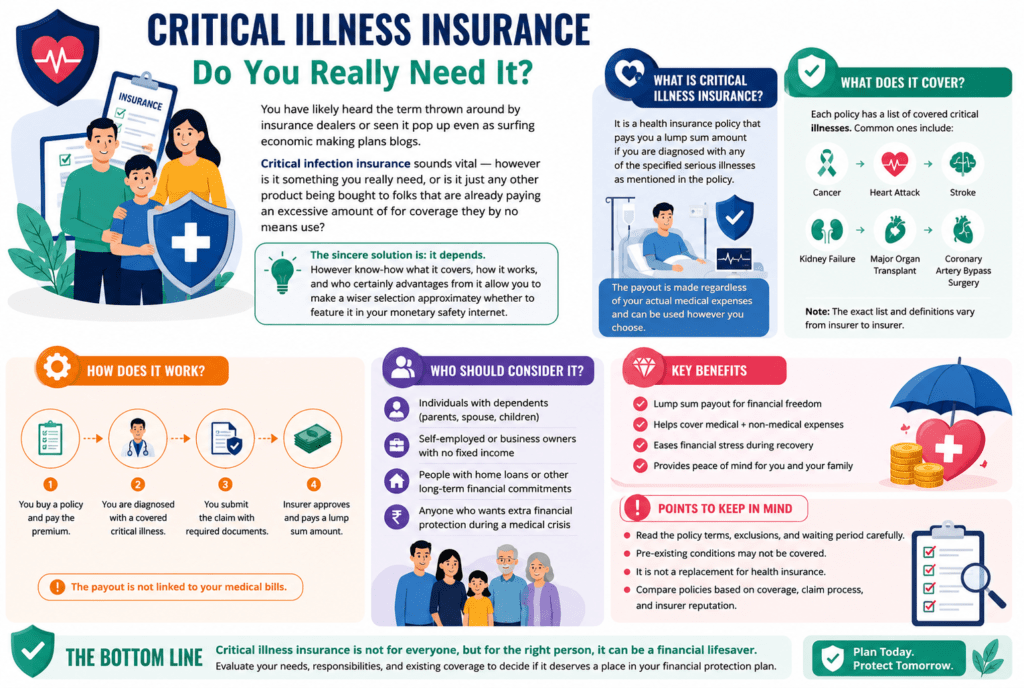

You have likely heard the term thrown around by insurance dealers or seen it pop up even while surfing economic planning blogs. Critical illness insurance sounds vital; however, is it something you really need? Or is it just any other product being bought by folks that are already paying an excessive amount for coverage they never use?

The sincere solution is: it depends. However, knowing what it covers, how it works, and who certainly benefits from it allows you to make a wiser selection about whether to include it in your financial safety net.

What is important contamination insurance?

Crucial infection insurance is a form of policy that pays out a lump sum of coins in case you are diagnosed with a severe medical condition indexed for your policy. Unlike conventional well-being protections. Which reimburses clinical carriers quickly for treatments, basic sickness protections put cash in your hands. No receipts required, no approval processes, no limitations on what you spend it on.

Commonplace conditions include coronary heart attack, stroke, cancer, kidney failure, and important organ transplants. And, from time to time, conditions like more than one sclerosis or Parkinson’s disease. The precise listing varies by using insurer and plan, so studying the exceptional print topics extraordinarily right here.

Whilst a covered diagnosis is shown, the insurer will pay your advantage, which would possibly range anywhere from $10,000 to $500,000, depending on your coverage, as a single, tax-free payment. You can use it to cover your health center deductibles, replace misplaced earnings whilst you get better, pay your loan, rent assistance at home, or even fly somewhere for specialised treatment.

The gap that makes this insurance relevant

Here is the hassle that critical infection coverage is designed to remedy: everyday health insurance can pay your doctors and hospitals, but it does not pay you.

While a person suffers a coronary heart attack or is diagnosed with cancer, the economic effect goes some distance beyond clinical payments. There are the misplaced profits at some stage in weeks or months, far away from work. There’s childcare that all of a sudden wishes to be organized. There’s the journey cost to a consultant three cities away. There may be an emotional and logistical toll that activates humans to spend money they in no way deliberate to spend.

Studies continuously show that clinical emergencies are one of the leading causes of private financial ruin. Even amongst humans who have medical health insurance. The payments get paid, however, the relaxation of existence continues costing money. And the general public’s financial savings aren’t constructed to absorb that type of sustained financial pressure.

This is the distance critical illness coverage fills.

Who benefits the most?

Now, not all and sundry desire a separate essential infection coverage with the same urgency. There are sure conditions where this insurance makes a whole lot of sense.

Self-hired individuals and freelancers are some of the highest-hazard institutions. If you don’t paint, you do not get paid. There is no organisation I’ll leave, no quick-term disability plan thru HR. And no person covers your half of the medical insurance while you are in a medical institution bed. A lump-sum payout may mean the difference between recovering in peace and watching your business disintegrate from a sanatorium room.

People with a family history of great infection ought to take this coverage seriously. If heart disease or most cancers have affected more than one generation in your family, the statistical probability of a claim is not just theoretical — it’s non-public. The younger and healthier you are when you buy the policy, the lower your premiums might be.

Individuals with high-deductible fitness plans also stand to gain significantly. These plans reduce your monthly premiums; however, they expose you to heaps of bucks in out-of-pocket costs when something major happens. An essential illness payout can cover that deductible after that, without draining your emergency fund.

Those with limited financial savings ought to recollect it too. Monetary advisors frequently suggest having three to 6 months of expenses in an emergency fund. The reality is that most families fall short of that. A severe infection that sidelines you for 6 months can wipe out anything reserve exists and put you into debt. Vital contamination coverage is, in a sense, a monetary backstop for the savings you have not constructed yet.

When it cannot be really worth it

There are valid reasons to pass this insurance or reprioritize it.

If you have extensive liquid savings — enough to cover six months or extra expenses with a few left over — you will be self-insured against the economic effect of an infection. The payout critical contamination coverage would provide doesn’t offer the same cost, whilst you already have resources to weather the hurricane.

If your agency gives robust long-term incapacity coverage, some of the income-alternative feature of critical illness insurance is already treated. Incapacity coverage replaces a portion of your earnings over the years, whereas vital infection gives you a lump sum in advance, but knowing what you already have in place enables clarify what’s missing.

You should additionally appearance cautiously at the exclusions. Pre-existing conditions are frequently excluded, which means coverage sold after you have already been recognized may not cover that diagnosis. A few regulations exclude early-stage cancers or only pay partial benefits for sure conditions. The coverage that looks lower priced may also cover far less than you count on, whilst it counts most.

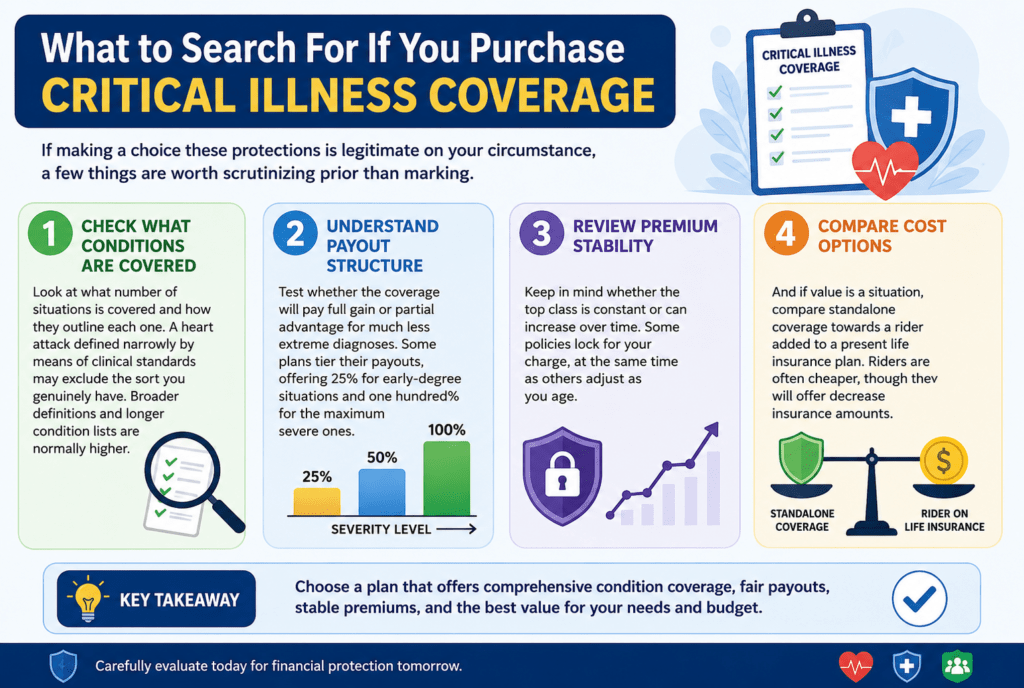

What to search for when purchasing

If making a choice, these protections are legitimate in your circumstance, a few things are worth scrutinizing prior to marking.

Look at the number of situations is covered and how they outline each one. A heart attack, defined narrowly by means of clinical standards, may exclude the sort you genuinely have. Broader definitions and longer condition lists are normally higher.

Test whether the coverage will pay full gain or partial advantage for much less extreme diagnoses. Some plans tier their payouts, offering 25% for early-degree situations and one hundred% for the maximum severe ones.

Keep in mind whether the top class is constant or can increase over time. Some policies lock for your charge, at the same time as others alter as you age.

And if the value is a situation, evaluate standalone coverage towards a rider added to a present life insurance plan. Riders are regularly cheaper, though they will offer decreased insurance amounts.

Conclusion

Vital contamination insurance isn’t always for everybody, but for a significant variety of people — especially the ones without a sturdy economic cushion, individuals who are self-employed, or people with multiple health dangers — it fills an actual and critical hole. It might not replace complete health insurance or a stable emergency fund; however, it is able to save you from a fitness crisis from turning into a financial disaster.

The query is not really whether or not critical infection insurance is worth having in concept. The question is whether or not the financial chance you would face without it is far worse than the one you may take without difficulty. For plenty of people, the sincere solution is not any, and that is when this coverage earns its place in a smart monetary plan.