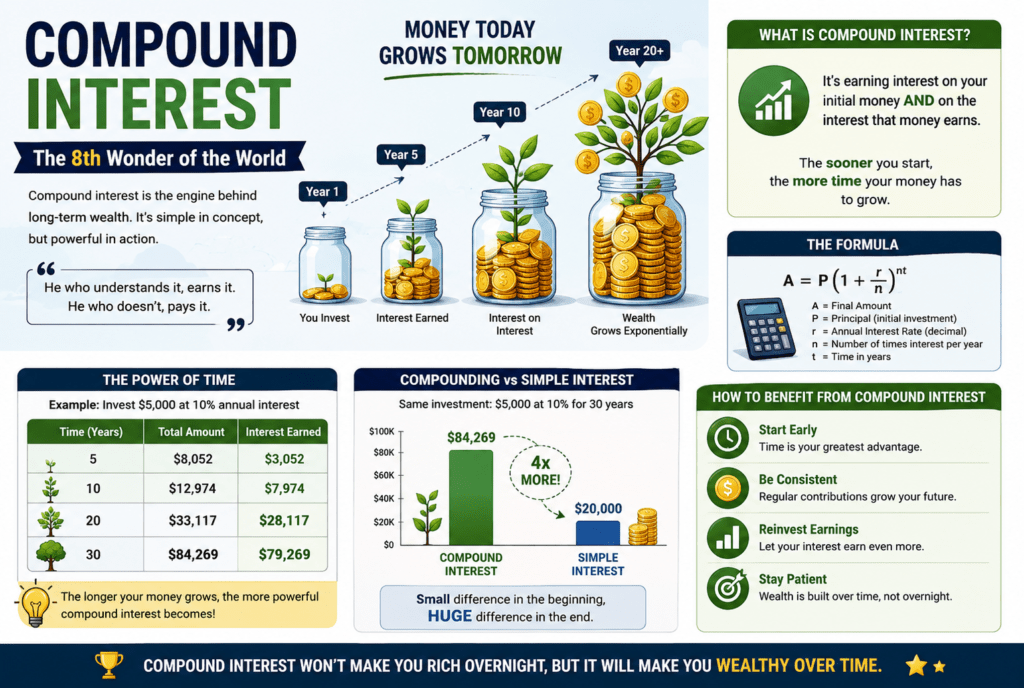

If there may be one economic idea that could certainly change the way you reflect on cash, it’s compound interest. Often referred to as the “8th wonder of the sector” — a word widely attributed to Albert Einstein, although its exact foundation is debated — compound interest is the engine at the back of long-term wealth creation. Whether or not you’re saving for retirement, building an emergency fund, or simply getting started on your economic adventure, knowing how compound interest works will let you make smarter decisions with each dollar you own.

What is a compound hobby?

To understand compound interest, you first want to apprehend its easier cousin: simple hobby. Simple interest is calculated on the actual amount of money you deposit or invest, referred to as the principal. If you make investments $1,000 at a five % annual simple interest rate, you earn $50 each year — no more, no less.

Compound hobby works in a different way. Rather than earning interest only in your main account, you earn hobby for your principal and on the hobby you’ve already accumulated. In other phrases, your interest starts offevolved earning hobby. That $1,000 at five % compounding every year becomes $1,050 after 12 months. In a year, you earn five % not on the unique $1,000, but on $1,050 — supplying you with $1,102.50. Every three hundred and sixty-five days, your balance grows a little faster than the 12 months before.

This could look like a small distinction at the start; however, over the years, the distance between simple and compound hobbies becomes great.

The power of Time

The maximum essential element in compound interest is time. The longer your cash compounds, the more dramatic the outcomes. This is why economic professionals continuously urge young people to begin saving and investing as early as possible — even though the amounts seem small.

remember human beings: Sarah and James. Sarah starts making a venture of $2 hundred per month at age 22 and stops at age 32 — contributing for fair 10 years. James waits until age 32 to start and invests $two hundred in line with month for 30 years instantly. Assuming both earn a median annual return of seven %, who finally ends up with more money at age sixty-two?

Sarah, despite investing for only 10 years, ends up with more. Her money had an additional decade to compound, and that head began to prove more powerful than James’s three additional years of contributions. This is the magic of compound hobby at work — time inside the marketplace regularly topics more than the amount invested.

How Compounding Frequency affects increase

Every other key thing is how often your hobby compounds. hobby can compound annually, quarterly, month-to-month, each day, or maybe constantly. The more frequently hobby compounds, the quicker your cash grows.

As an instance, $10,000 invested at a 6% annual interest rate will develop in a different way depending on compounding frequency:

- Compounded annually: ~$17,908 after 10 years

- Compounded monthly: ~$18,194 after 10 years

- Compounded every day: ~$18,221 after 10 years

The variations would possibly appear small in a decade, but stretch that out to 30 or 40 years, and the gaps widen drastically. Whilst selecting financial savings, money owed or investment vehicles, always be aware of whether or not interest compounds every day or monthly — it subjects more than the majority recognize.

The rule of 72

One of the easiest methods to estimate how long it’s going to take for your money to double is the rule of thumb of seventy-two. Surely divide seventy-two by your annual hobby charge, and the end result offers you the approximate range of years it’ll take to double your investment.

A 6% annual return, your money doubles kind of each 12 years (seventy two ÷ 6 = 12). At nine percent, it doubles every 8 years. At four percent, it takes about 18 years. This simple intellectual shortcut will let you quickly examine investment opportunities and set realistic economic expectations without having a calculator.

In which Compound interest Works for You

Compound interest is at play in numerous commonplace monetary products. excessive-yield financial savings, money owed, certificates of deposit (CDs), cash market money owed, and investment portfolios all benefit from compounding. Retirement accounts like 401(k)s and IRAs are particularly effective due to the fact that they allow your investments to compound over a long time, while additionally presenting tax advantages.

The inventory market, even as no longer technically a “hobby,” offers a compounding effect via reinvested dividends and capital appreciation. Many long-term buyers reinvest dividends routinely, which turbocharges growth over the years. Index finances and ETFs are popular gear for having access to this type of wide-market compounding without the need to pick individual shares.

Whilst Compound hobby Works in opposition to You

It’s far more vital to remember that compound interest is a double-edged sword. The equal pressure that grows your financial savings can also grow your debt — and it does so simply as aggressively.

Credit card balances are a top example. With average interest rates often sitting above 20%, carrying a balance does not just cost you the interest on what you borrowed. It costs you a hobby in your developing interest as well. A $three,000 credit card balance at 22% APR, if left unpaid and only minimal payments are made, can take well over a decade to pay off and cost hundreds of dollars in more fees.

Scholar loans, car loans, and private loans also compound, although commonly at lower rates. Information, this is not supposed to frighten you — it is supposed to inspire, spark off compensation, and discourage sporting high-interest debt longer than necessary.

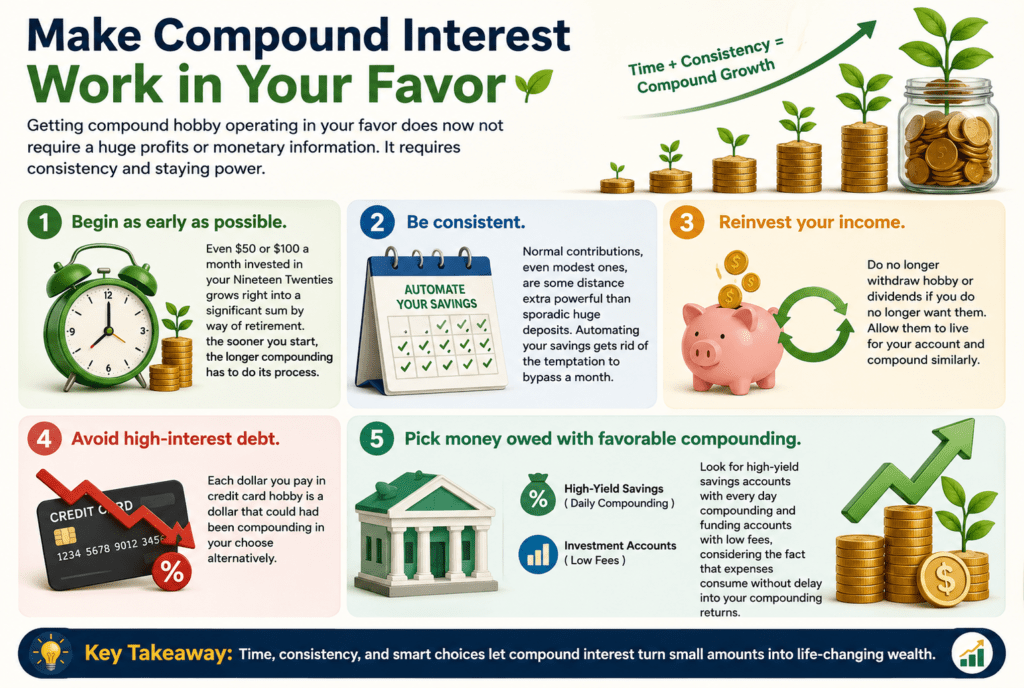

Sensible Steps to Make Compound interest be just right for You

Getting a compound hobby operating in your favor does not require huge profits or financial information. It requires consistency and staying power.

- Begin as early as possible. Even $50 or $a hundred a month invested in your Nineteen Twenties grows right into a significant sum by way of retirement. The sooner you begin, the longer compounding has to do its process.

- Be consistent. Normal contributions, even modest ones, are some distance extra powerful than sporadic huge deposits. Automating your savings gets rid of the temptation to bypass a month.

- Reinvest your income. Do no longer withdraw hobby or dividends if you do no longer want them. Allow them to live for your account and compound similarly.

- Avoid high-interest debt. Each dollar you pay in credit card interest is a dollar that could have been compounding in your account alternatively.

Pick money owed with favorable compounding. Look for high-yield savings accounts with everyday compounding and funding accounts with low fees, considering the fact that expenses consume without delay into your compounding returns.

Conclusion

Compound hobby isn’t a get-rich-quick scheme — it’s a get-wealthy-slowly approach that surely works. The approach is easy: begin early, live consistently, avoid unnecessary debt, and let time do the heavy lifting. Whether or not you have got $100 or $a hundred,000 to make investments, the principles continue to be the same. Your destiny self will thanks for the discipline you display today.